How an Insurance Claims Platform Improves Triage and Visibility

I’ll start with the slightly spicy take: most claims teams do not have a triage problem because their adjusters lack judgment. They have a triage problem because the claim arrives half-blind.

A photo sits in one system. A police report is attached to an email. Coverage notes live in the core system. Prior loss history may or may not have been checked. Then we ask an adjuster, often before coffee, to decide what needs attention first. That is not triage. That is office archaeology.

A good insurance claims platform changes that. It brings the claim, the context, the routing logic, and the operational view into one working layer so teams can answer the two questions that matter most in the first few minutes: “What is this claim?” and “What should happen next?”

I learned this lesson the unglamorous way. Years ago, during a nasty hail season, I watched a claims supervisor triage new losses with three browser tabs, a spreadsheet, sticky notes, and the confidence of someone defusing a bomb with a butter knife. She was excellent. The process was not. The problem was not effort. It was visibility.

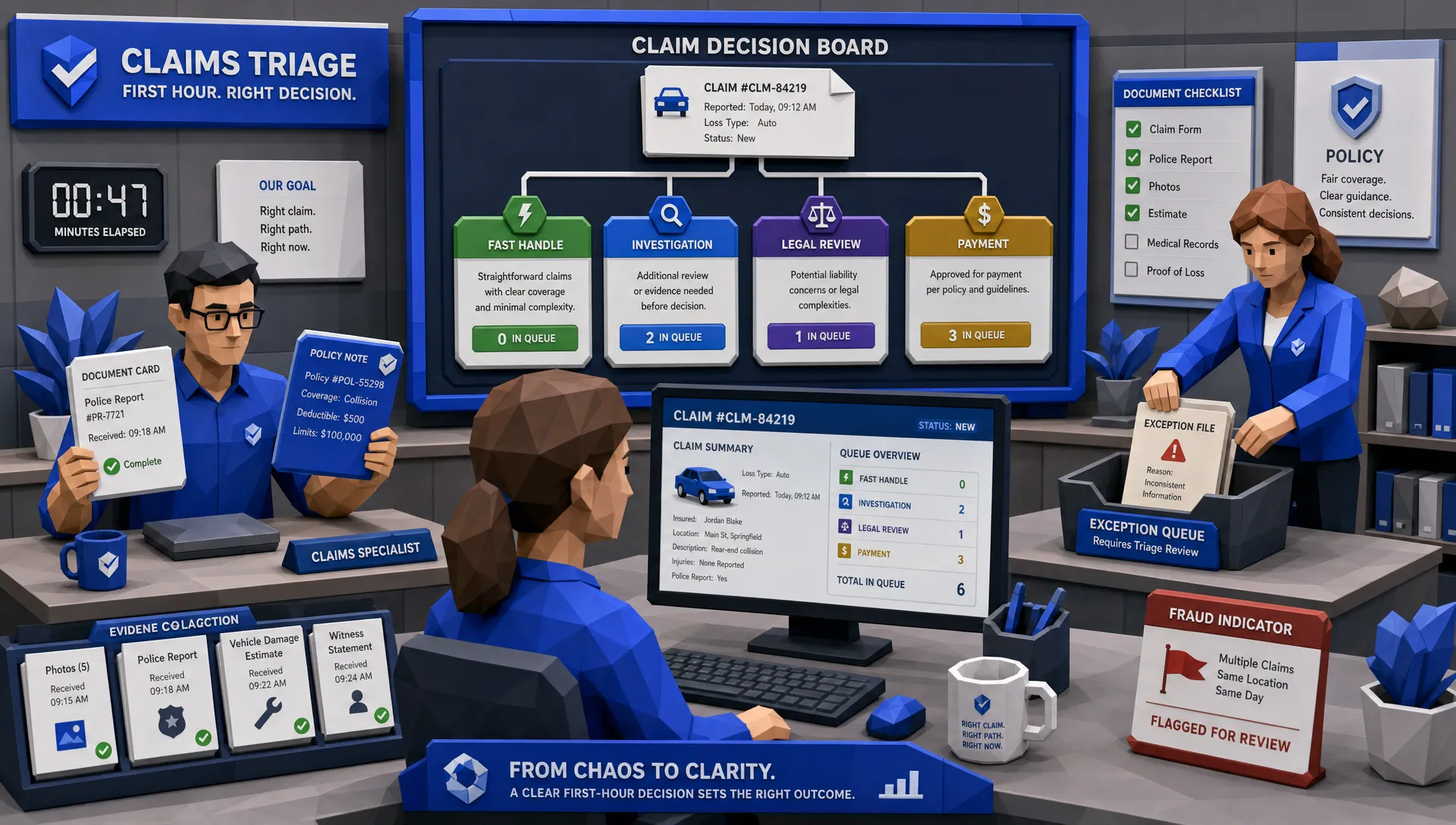

The First Hour of a Claim Is Where the Tone Gets Set

The first hour after FNOL is more important than we like to admit. That is when the claim is categorized, coverage is checked, documents are requested, severity is estimated, fraud indicators are noticed or missed, and the file is assigned.

When that first hour is messy, the rest of the claim inherits the mess. A simple windshield claim waits behind a bodily injury file. A represented claimant sits in a general queue. A suspicious loss gets treated like routine damage until someone spots the pattern three weeks later. None of this feels dramatic in the moment. It becomes expensive quietly.

J.D. Power’s 2024 U.S. Auto Claims Satisfaction Study highlights how long cycle times and poor communication continue to frustrate claimants. Anyone who has worked claims knows the painful truth behind that data: many delays are not caused by the repair, the inspection, or the settlement decision. They are caused by waiting for someone to realize what the file needs.

That is where triage should earn its keep.

A modern insurance claims platform improves triage by making the claim readable from the start. It captures FNOL data consistently, pulls in policy and customer details, organizes documents, and applies routing rules based on the nature of the loss. The goal is not to remove judgment from claims handling. The goal is to stop wasting judgment on basic sorting.

Triage Is Not a Queue, It Is a Decision System

Here is another hot take: if your triage process is mainly a shared inbox, you do not have a triage process. You have a digital waiting room.

Real triage considers severity, complexity, coverage status, jurisdiction, litigation risk, fraud signals, customer profile, policy conditions, and operational capacity. A low-value claim can still be urgent if the customer is stranded. A high-value claim can still be routine if the facts are clean and documentation is complete. A bodily injury claim with attorney involvement should never be treated like a standard property damage file simply because both arrived on Tuesday.

This is where automation helps most. Not by pretending every claim can be settled without a human, but by sorting claims into the right path faster. Some claims should move toward straight-through processing. Some need an experienced adjuster. Some need SIU attention. Some need legal review. Some need a missing document before anything useful can happen.

Celent has reported that only a small share of claims are processed straight-through without human intervention, often in the 10% to 15% range, depending on line and insurer maturity, according to its work on straight-through processing in claims. That matches what I have seen in practice. The dream of every claim running itself is not realistic for most carriers and MGAs. The practical win is knowing which claims can move quickly and which need skilled hands immediately.

If you want to go deeper on the scoring and routing side, we have covered how predictive analytics improves triage by helping teams identify the next best action earlier in the process.

Visibility Is More Than a Dashboard With Nice Colors

I have nothing against dashboards. I enjoy a neat chart as much as the next recovering spreadsheet addict. But claims visibility is not about admiring graphs in a leadership meeting. It is about knowing what is happening while there is still time to act.

A useful insurance claims platform gives visibility at several levels. At the claim level, an adjuster can see what is missing, what has been completed, who owns the next step, and whether the claim is drifting from the expected path. At the queue level, supervisors can see workload, aging, bottlenecks, and escalation patterns. At the portfolio level, leaders can see trends across severity, cycle time, vendor performance, litigation exposure, and leakage.

The difference is timing. A monthly report tells you where the barn burned down. Operational visibility tells you where smoke is starting.

This matters because claims organizations are full of small waiting states that are hard to see from the outside. A file waits for a document. A vendor waits for assignment. An adjuster waits for coverage confirmation. A claimant waits for a call. The claim does not look “stuck” because technically someone is assigned. But from the customer’s perspective, nothing is moving.

A platform that connects claim activity, documents, policy data, and workflow status can expose those waiting states before they become complaints. That is the difference between managing work and chasing work.

Connected Data Is the Foundation

Claims visibility falls apart when data is scattered. I have seen teams with good people, good intentions, and terrible visibility because every answer required a treasure hunt. One system had the policy. Another had claim notes. Another had documents. Fraud checks lived somewhere else. Reporting came later, usually after someone exported a CSV and prayed.

An insurance claims platform should reduce that fragmentation. Inaza, for example, is built around a unified data warehouse that supports workflow automation, reporting, and analytics. That matters because the workflow is only half the story. The data created by the workflow is what helps leaders understand performance.

If your platform captures every important claims event, intake field, enrichment result, assignment, status change, and outcome, you can do much more than move work faster. You can ask better business questions. Where are claims aging? Which claim types generate rework? Which jurisdictions are trending worse? Which vendors are slowing settlements? Which adjusters need support, and which workflows need redesign?

We have written more about why connected claims data is the real backbone of better claims operations. Without connected data, even the sharpest triage logic is working with one eye closed.

Fraud and Litigation Signals Need to Appear Early

Fraud and litigation exposure are two areas where late visibility is especially painful. By the time a suspicious claim has bounced through three handlers, or an attorney demand has surprised the team, the carrier may already be on the back foot.

The scale is not small. The FBI estimates insurance fraud costs the United States more than $300 billion annually. Meanwhile, Verisk’s 2025 fraud report points to rising concern around digital fraud and the use of generated or manipulated evidence. Claims teams do not need more paranoia. They need earlier signals.

That means triage should not stop at “auto physical damage” or “property water loss.” It should surface context. Is there prior claims activity? Is the loss description inconsistent with the documents? Is attorney involvement present? Are images, invoices, or medical documents behaving oddly? Is the claim type known to produce leakage in a certain region?

A claims platform can help by bringing those indicators into the routing process. The result is not a magic fraud detector. The result is earlier attention from the right people. That is far more valuable than discovering concerns after payment has been made or litigation posture has hardened.

Claims Can Learn From Other Signal-Driven Teams

Insurance sometimes acts like it invented operational complexity. We did not. Sales, logistics, banking, healthcare, and customer support all deal with high-volume workflows where signals determine urgency.

A sales operations team would never tolerate a lead system that hides source, status, risk, and next action. That is why tools such as autonomous B2B prospecting platforms focus on detecting signals, enriching records, and triggering the next step. Claims has a different mission, of course, but the operating lesson is similar: work improves when signals are visible and action is guided.

In claims, those signals are not buying intent. They are coverage issues, severity indicators, missing information, fraud markers, litigation risk, customer vulnerability, and operational bottlenecks. When those signals are visible early, triage becomes much more than sorting. It becomes control.

What to Look For in an Insurance Claims Platform

If I were evaluating an insurance claims platform today, I would care less about the flashiest demo and more about whether it can survive contact with real claims work.

First, it should integrate with existing systems. Most insurers are not replacing every core platform next quarter, and frankly, they should not have to. The claims layer needs to connect to what is already there, pull the right information, and push updates back where needed.

Second, it should handle messy inputs. Claims arrive as PDFs, emails, forms, photos, spreadsheets, medical bills, legal letters, and sometimes documents that look like they were scanned during an earthquake. A platform that only works when data is clean will disappoint you by lunchtime.

Third, it should let teams configure workflows without turning every change into a six-month project. Claims operations change constantly. A new attorney pattern appears. A storm event hits. A state regulation changes. A carrier launches a new program. If workflow updates require endless back and forth, the business will route around the system.

This is an area where Inaza is intentionally practical. The platform supports customizable automation workflows, 250-plus workflow templates, all file types, and integrations with existing systems. It also includes pre-built API templates for data enrichment providers such as Verisk, LexisNexis, and HazardHub. That combination matters because triage improves when the platform can collect, enrich, route, and report without forcing claims teams to relearn their jobs.

Fourth, the platform should turn workflow activity into business intelligence. A task tool can tell you a file moved. A claims data platform can tell you why files are moving slowly, where leakage appears, and how performance compares against internal goals or market benchmarks. Inaza’s approach includes real-time analytics dashboards and benchmark context, which can support stronger portfolio narratives for renewals, reinsurance discussions, and executive reviews.

The Human Side: Better Triage Makes Adjusters Better

One concern I hear from claims teams is that automation will turn adjusters into button-clickers. I understand the concern. Claims is a judgment business, and nobody wants good adjusters treated like conveyor belt operators.

But in my experience, poor triage is what actually drains adjuster judgment. It gives experienced people routine files that could have moved faster. It gives junior handlers complex files before they are ready. It buries urgent work beneath easy work. It forces supervisors to act like air traffic controllers with fogged-up windows.

Better triage does the opposite. It protects adjuster time for decisions that deserve human expertise. It gives new handlers clearer guardrails. It gives supervisors visibility before problems pile up. It gives customers faster answers when their claim is simple, and more experienced attention when their claim is not.

The best insurance claims platform is boring in the nicest possible way. It gives each file a clean record, a clear owner, a sensible path, and enough visibility that nobody has to ask, “Where did this claim go?”

Frequently Asked Questions

What is an insurance claims platform? An insurance claims platform is a system that helps insurers manage claims intake, triage, assignment, documentation, workflow, reporting, and analytics. Modern platforms often connect with existing core systems rather than replacing them entirely.

How does an insurance claims platform improve triage? It improves triage by collecting claim information consistently, enriching it with relevant data, identifying severity or fraud indicators, and routing the file to the right team, adjuster, vendor, or review path earlier.

Does claims automation replace adjusters? No, not in any serious claims operation. The real value is removing manual sorting, data capture, and repetitive handoffs so adjusters can spend more time on judgment, negotiation, customer communication, and complex coverage issues.

Why is visibility so important in claims management? Visibility helps teams see aging claims, missing information, workload imbalance, escalation risk, and bottlenecks before they become customer complaints, leakage, or litigation problems.

What should insurers prioritize when choosing a claims platform? Prioritize integration with existing systems, flexible workflow configuration, support for multiple file types, reliable data enrichment, clear dashboards, and the ability to turn claims activity into useful business intelligence.

Make Triage Visible Before It Gets Expensive

Claims teams do not need another pretty screen that tells them yesterday was busy. They need a working platform that shows what each claim needs now, where it should go next, and which risks deserve attention before they become costly.

That is the practical promise of a modern insurance claims platform: cleaner triage, better visibility, fewer blind spots, and more time for claims professionals to do the work that actually requires experience.

If your team is ready to improve claims workflows without ripping out existing systems or retraining everyone from scratch, Inaza can help you automate intake, triage, reporting, and analytics in a way that fits real insurance operations.