Claims Automation Software Buyers Ask the Wrong Questions

Here is my mildly spicy take after a decade around insurance operations: most claims automation software buying conversations start in the wrong place.

We ask, “Can it read PDFs?” We ask, “Does it integrate with our core system?” We ask, “How many claims can it process per hour?” Fair questions, sure. But they are the appetizer, not the meal.

The better question is this: will this system improve claim decisions, reduce avoidable touchpoints, and leave us with cleaner data than we had yesterday?

I have sat in enough claims transformation meetings to know the pattern. A vendor shows a beautiful demo. A claim comes in, documents are classified, a payment recommendation appears, everyone nods, and someone says, “Looks great, but can it handle our edge cases?” That question usually arrives 48 minutes too late.

Claims automation software should not be judged by how elegantly it handles the easy claim. Easy claims have always been easy. The real test is what happens when the police report is missing, the claimant’s story changes, the estimate does not match the photos, the attorney demand arrives at 4:57 p.m. on Friday, and your adjuster has six other fires burning.

The wrong question sounds reasonable

Most buyers are not asking bad questions because they lack experience. They are asking bad questions because software demos train us to think in features.

Feature questions feel safe. They are specific, they fit nicely into RFP spreadsheets, and they give procurement something to compare. The trouble is that claims is not a spreadsheet sport. Claims is judgment, documentation, compliance, empathy, negotiation, leakage control, fraud detection, and timing, all happening under pressure.

Here is the shift I wish more carriers, MGAs, and TPAs would make earlier in the process.

Common buyer question | Better buyer question | Why it matters

Can it automate FNOL? | Which intake fields improve downstream decisions? | Intake is only useful if it reduces later rework.

Does it use AI? | What decisions does it support, and what decisions stay with an adjuster? | Automation without boundaries creates operational risk.

Does it integrate with our core system? | Can it work with our current systems without forcing a rebuild? | Most insurers live with mixed technology stacks. That is reality.

How fast is implementation? | How fast can we get a controlled workflow into production? | A quick demo is not the same as a live operating process.

What is the cost per claim? | Which expense, leakage, and cycle-time metrics will change? | Cheap software that moves the wrong work faster is still expensive.Ask which claims should not go straight through

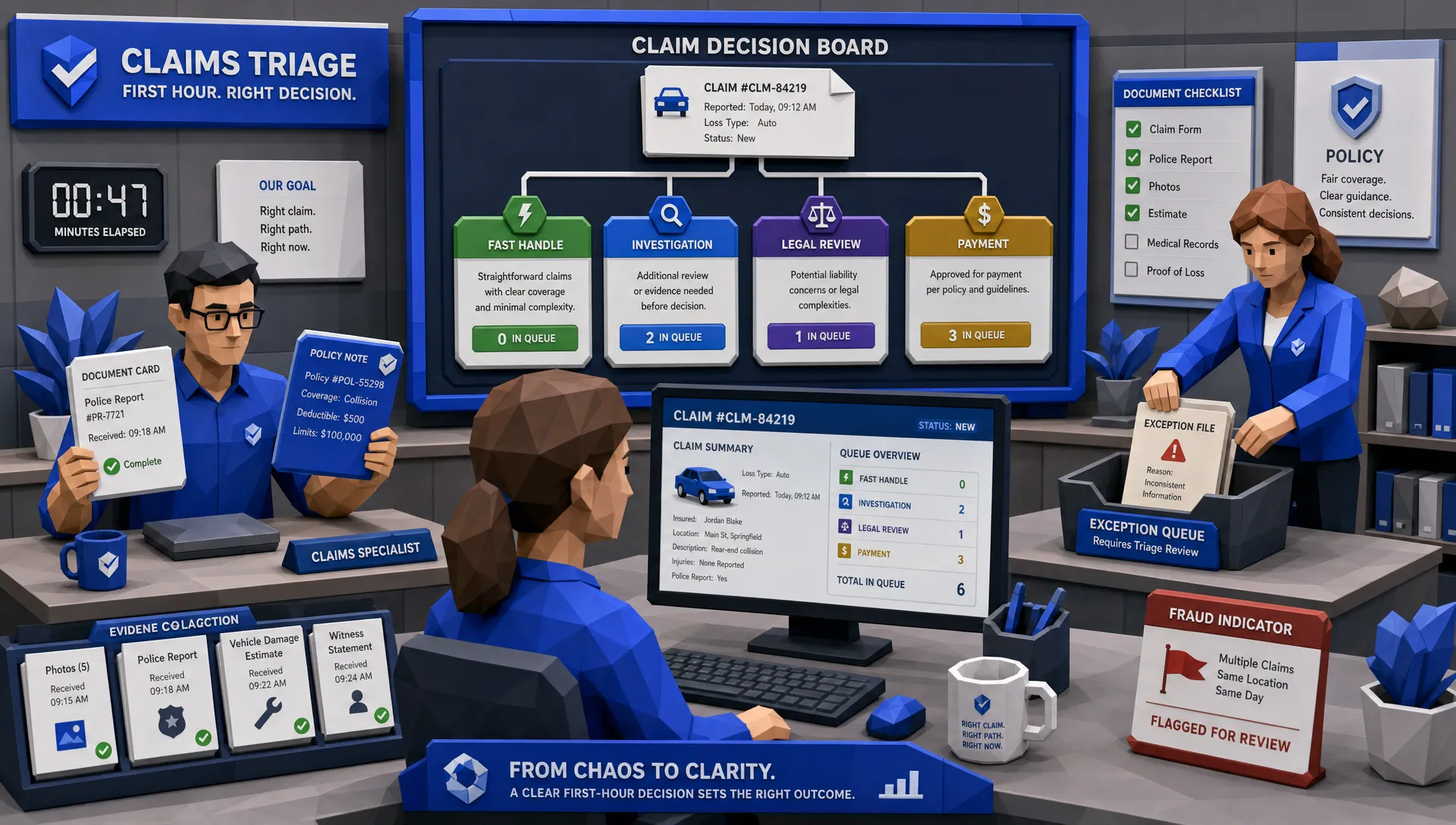

Straight-through processing sounds wonderful until you ask, “Straight through to where?”

A low-severity windshield claim with clean coverage and no suspicious signals may deserve a near-touchless path. A bodily injury claim with conflicting facts does not. A represented claimant with a demand package needs a very different control structure. A CAT claim might need fast triage, but it also needs careful severity detection.

Celent has reported that only a small share of claims, often cited around 10% to 15%, are processed straight through without human intervention. That tracks with what I have seen in the field. The dream is not to make every claim touchless. The dream is to stop wasting skilled adjuster time on tasks that do not require skill.

A better claims automation software discussion starts by sorting claims into operating lanes.

Claim scenario | Sensible automation posture | Human role

Simple, low-severity, clean documentation | Automate intake, validation, routing, communication, and payment recommendation | Review exceptions and monitor quality

Missing documents or incomplete facts | Automate follow-up requests and diary management | Decide whether the file can proceed

Potential fraud indicators | Automate signal detection and referral packaging | Investigate, document, and decide next action

Attorney-represented demand | Automate extraction, chronology, and reserve support | Evaluate liability, damages, negotiation posture

Complex coverage or high severity | Automate data gathering and summaries | Own coverage, strategy, and settlement judgment Ask whether the software improves the claim file

A lot of automation tools move tasks around. Fewer improve the underlying claim file.

That distinction matters. A clean claim file helps the adjuster, supervisor, SIU team, reinsurer, auditor, and defense counsel. A messy file with faster routing is still a messy file. It just arrives faster and annoys everyone sooner.

Years ago, I watched an adjuster handle a relatively simple auto property damage claim. The file had the estimate in one system, photos in another, a police report attached to an email thread, and a coverage note buried in free text. The actual decision was not complicated. Finding the facts was the job. That is where operational expense hides, in the scavenger hunt.

Good claims automation software should capture and structure the facts while the work happens. That means extracting key dates, parties, coverage indicators, loss descriptions, injury mentions, repair amounts, attorney involvement, prior claims indicators, and missing items. It should also create an audit trail that a supervisor can understand without needing three cups of coffee and a treasure map.

This is why I like to separate “workflow automation” from “file intelligence.” Workflow automation says, “Move this claim to the next step.” File intelligence says, “Here is what we know, here is what we do not know, here is what changed, and here is why the next step makes sense.”

If your team keeps circling back to the same missing facts, coverage questions, and status updates, Inaza has a useful breakdown of the claims questions that slow teams down. In my experience, those recurring questions are often the best roadmap for what to automate first.

Ask how it handles the weird stuff

Every claims leader has a favorite “you will not believe this one” story. Mine involved a vehicle damage photo that looked suspiciously like it had been generated by a toaster with artistic ambitions. The adjuster spotted it because the shadowing was wrong and the license plate reflection made no sense. Technology did not catch it. A tired human did.

That story used to be funny. It is becoming less funny.

The FBI notes that insurance fraud costs U.S. consumers more than $40 billion per year, excluding health insurance. Verisk’s 2025 fraud reporting also highlights how digital tools are raising concern among carriers, including manipulated images and fabricated claim materials. Fraud has always adapted to the claim process. When the process becomes digital, fraud adapts there too.

So do not only ask whether claims automation software can process standard documents. Ask how it handles contradiction, uncertainty, and suspicious patterns. Can it compare the loss description to photos? Can it flag mismatches between estimate line items and visible damage? Can it identify duplicate documents or unusual timing? Can it package a referral so SIU gets a useful file rather than a vague “please review” note?

The best automation does not replace skepticism. It gives skepticism better evidence.

Ask where the money will actually show up

“Efficiency” is one of those words we all use when we want to sound responsible without committing to a number. I have used it myself. Guilty as charged.

But claims automation buyers need to be more specific. Are we trying to reduce loss adjustment expense? Improve cycle time? Reduce leakage? Improve customer satisfaction? Increase adjuster capacity? Catch fraud earlier? All of the above sounds nice, but the business case needs a primary target.

J.D. Power’s 2024 U.S. Auto Claims Satisfaction Study reinforces what claims people already know in their bones: cycle time and communication shape the customer experience. A claimant who hears nothing for ten days does not care that your internal routing logic improved by 18%. They care that nobody told them what happens next.

A serious buyer should define the value pool before the demo.

Value area | What to measure | What good automation changes

Cycle time | FNOL to assignment, first contact, coverage decision, settlement | Removes waiting, chasing, and manual routing

Expense | Adjuster touches, rework, vendor follow-ups, supervisor escalations | Reduces low-value manual handling

Leakage | Reserve changes, missed subrogation, duplicate payments, late fraud referrals | Surfaces facts and inconsistencies earlier

Customer experience | Status calls, complaints, digital response time, satisfaction scores | Gives customers timely and accurate updates

Compliance | Diary adherence, documentation completeness, audit exceptions | Makes required steps visible and repeatable Ask whether it can live with your legacy reality

I have yet to meet an insurer with a perfectly clean technology environment. Somewhere there is a core system that has been customized since the Clinton administration, a reporting database nobody wants to touch, and a spreadsheet called “FINAL_final_v7.” If you are smiling, I am sorry. Also, I see you.

Claims automation software must work with that reality. A rip-and-replace project may be appropriate in some cases, but most claims leaders need practical progress long before a core modernization program reaches the finish line.

This is why integration questions should go deeper than “Do you have APIs?” Ask what file types the software can ingest. Ask how it handles email attachments, PDFs, images, loss runs, police reports, repair estimates, medical bills, and demand letters. Ask whether it can enrich data from third-party sources. Ask whether the claims team can keep working in familiar systems while automation handles the repetitive steps around them.

We have covered this in more detail in our article on why legacy systems should not hold back claims automation. The short version: legacy systems are a constraint, not an excuse. Good automation wraps around the real operating environment instead of demanding a fantasy version of it.

Ask what happens after the demo

The insurance industry has a strange fondness for pilot projects. I understand why. Nobody wants to bet the claim operation on a vendor promise. But pilots can become theater if they are not tied to production readiness.

Here is the question I would ask every vendor: “Can we build a real workflow with our actual claims process, our actual documents, and our actual controls, then put it in front of users without six months of back-and-forth?”

That answer matters more than a polished demo. Claims processes change. CAT events change volume overnight. Plaintiff attorney tactics change. Regulatory expectations change. New product lines come in. A workflow that requires a consulting project every time something changes will eventually become shelfware with a login page.

This is one reason Inaza’s approach is built around configurable workflows, a unified data warehouse, and pre-built templates for insurance processes. The point is to help insurers, MGAs, and brokers deploy useful automation faster, capture the data created by that automation, and turn it into reporting and analytics. Inaza also supports enrichment through pre-built API templates, including sources such as Verisk, LexisNexis, and HazardHub, which can matter when claim decisions depend on external facts.

The unglamorous part is often the most valuable part: once the workflow is live, the data it produces should help leaders see bottlenecks, exceptions, leakage patterns, and operational performance. If automation does not improve management visibility, it is leaving half the value on the table.

For a broader view of the operating controls that matter, I recommend this piece on what matters most when automating insurance claims processing. It gets to the heart of the issue: the workflow is only as good as the data, handoffs, and controls underneath it.

A better buyer scorecard for claims automation software

If I were buying claims automation software tomorrow, I would still look at features. I am not a complete rebel. But I would score the vendor on evidence, not adjectives.

Buyer test | What to ask for

Claim segmentation | Show which claim types should be automated, assisted, or excluded.

Data quality | Show the structured fields created from real claim documents.

Exception handling | Show what happens when information is missing, conflicting, or suspicious.

Adjuster experience | Show the adjuster view, not only the executive dashboard.

Integration reality | Show how the software works with current systems and file types.

Controls and auditability | Show who approved what, when, and based on which facts.

Reporting value | Show how operational data becomes useful management insight.

Speed to production | Show a path from workflow design to live use, not only a sandbox demo. Frequently Asked Questions

What is the biggest mistake buyers make with claims automation software? The biggest mistake is evaluating feature lists before defining claim outcomes. Buyers should decide whether they are targeting cycle time, expense, leakage, fraud referrals, compliance, customer communication, or adjuster capacity before comparing vendors.

Should claims automation software fully replace adjusters? No. The strongest use case is usually removing repetitive administrative work so adjusters can focus on judgment, negotiation, coverage, severity, and customer communication. Full automation makes sense for some simple claims, but complex files still need human ownership.

Can claims automation work with legacy claims systems? Yes, if the software is designed to integrate with existing systems and handle real-world file types. Buyers should ask how the platform ingests documents, exchanges data, and supports users without requiring a full core system replacement.

How should insurers measure success after implementation? The best measures include cycle time, adjuster touches, rework, documentation completeness, fraud referral quality, customer status calls, settlement delays, and audit exceptions. Pick the metrics that match the business case before deployment.

What should be automated first in claims? Start with repetitive work that slows decisions, such as intake validation, document classification, missing information requests, routing, status updates, and data enrichment. Avoid starting with the most complex claim decisions unless the controls are very clear.

Stop buying workflows. Start buying claims outcomes

The wrong questions make claims automation software look like a feature race. The right questions make it an operating decision.

Can it improve the claim file? Can it guide the right work to the right person? Can it spot exceptions without pretending every file is simple? Can it work with the systems you already have? Can it produce data that leadership can actually use?

That is the conversation worth having.

If your claims operation is ready to move beyond demo theater and into production-ready automation, Inaza can help you build workflows that fit your process, connect with your systems, and turn claims activity into useful operational intelligence.