Why Underwriting Software for Insurance Fails on Messy Files

My hot take: most underwriting software for insurance does not fail because underwriting is too complex. It fails because the files are ugly.

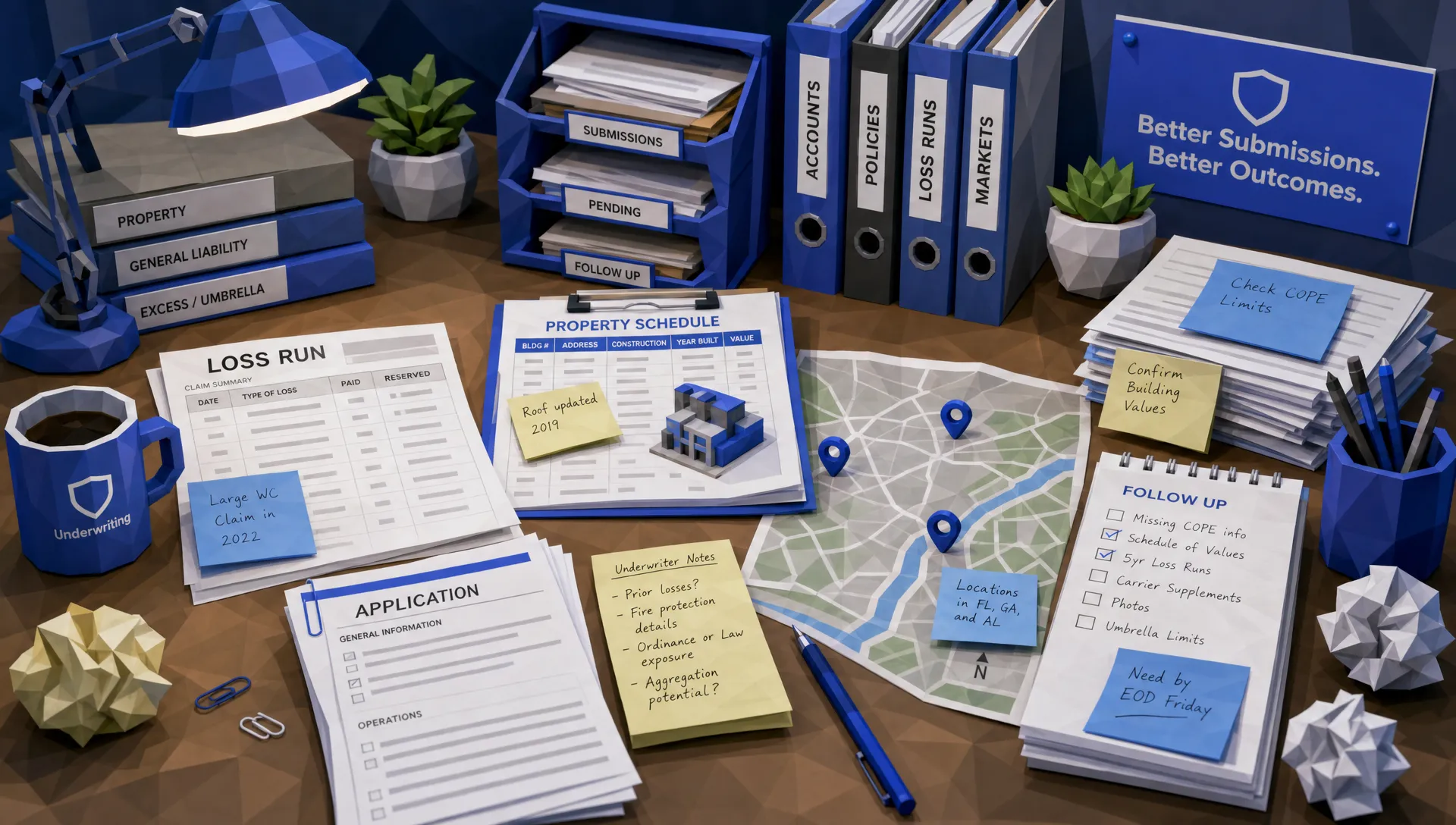

I have seen beautiful demo environments collapse the moment a real submission arrives. You know the one. A broker email with the subject line “Updated final version,” three PDFs named “New New,” an Excel schedule with hidden tabs, a loss run scanned sideways, and a note in the body that says, “Same as expiring, except the roof and the payroll.”

That is not an edge case. That is Tuesday.

The uncomfortable truth is that underwriting still runs on documents, emails, attachments, and half-structured clues. If software cannot handle messy files, it cannot handle underwriting. It may still look impressive in a boardroom, but the underwriter will be back to copy-paste, tab-hopping, and muttering into their coffee by lunch.

Messy files are not a small intake problem

We tend to talk about messy files as if they are a front-door issue. Clean up intake, problem solved. I agree that intake matters, and we have written before about why insurance underwriting software fails without good intake. But messy files deserve their own conversation because they do not stop being messy after they enter the system.

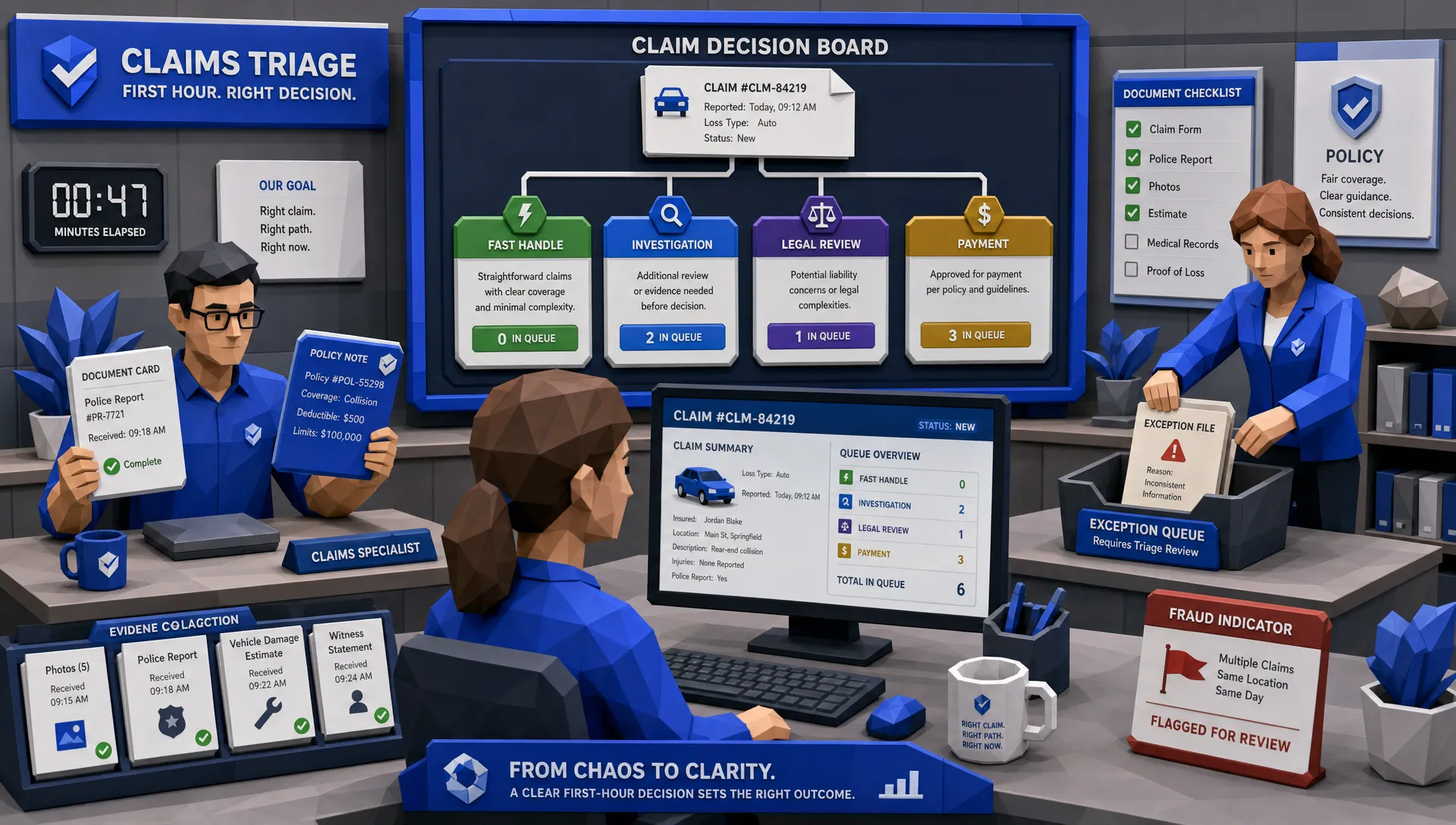

They follow the submission through triage, clearance, rating, referral, quote, bind, audit, renewal, reporting, and sometimes claims. One bad file can create six bad decisions.

McKinsey has estimated that underwriters spend a large share of their time on administrative work rather than risk assessment, with automation offering a major opportunity to change that pattern. Anyone who has worked a new business rush in commercial lines knows exactly what that looks like. The work is not always “underwriting” in the pure sense. It is finding the right address, checking whether the loss run is current, comparing payroll across two documents, and figuring out whether the broker’s note overrides the PDF.

This is why messy-file handling is not a nice-to-have. It is the core job.

Why clean-demo software breaks in the real world

Most underwriting software demos are based on polite data. Every field has a label. Every file has a purpose. Every document arrives in the correct order, like it was raised in a Swiss finishing school.

Real submissions behave more like toddlers with permanent markers.

The first failure is usually file recognition. The system can accept a PDF, sure, but can it tell the difference between a statement of values, a loss run, a supplemental application, a driver schedule, a prior quote, and a broker cover note? Can it split a 90-page attachment into useful sections without asking a human to do the tedious work first?

The second failure is contradiction. A file says the insured has five locations. Another says seven. The email mentions a newly acquired site. The schedule of values has six rows, but one row has no address. A weak system picks one value and moves on. A useful system flags the conflict, shows the source, and routes the issue to the right person.

The third failure is source traceability. If an underwriter asks, “Where did that number come from?” the answer cannot be “the system found it.” That answer would last about twelve seconds in a referral meeting. Underwriters need to see the document, page, field, timestamp, and confidence behind the extracted data.

The fourth failure is version control. If you have never bound a risk based on a stale attachment, congratulations, you have either been lucky or you have a very tidy broker panel. For the rest of us, file versions matter. Newer is not always better, either. Sometimes the “final” file is missing the tab that was in the earlier version.

The file is often the evidence

Here is where I get a bit opinionated. A lot of underwriting technology treats documents as something to be converted into data and then discarded. That is a mistake.

In insurance, the document is often evidence. It carries context, intent, and sometimes legal weight. The wording in a broker email matters. A signed supplemental matters. A scanned inspection note with a handwritten comment can matter. If the system extracts the value but loses the trail, it has created a new risk while trying to reduce an old one.

I once saw a small account referral turn into a mini-detective story because the occupancy description changed between two documents. The system of record had one value, the PDF had another, and the broker’s email had a third. The real answer was buried in an attachment named, I kid you not, “Use this one maybe.” That account was not huge, but the process told us everything we needed to know about the software around it.

Good underwriting systems should respect the file as part of the underwriting record, not just as raw material for a database.

OCR is not enough

There is a common misconception that messy-file handling equals OCR. If the software can read text from a PDF, the thinking goes, the job is done.

Not quite.

OCR is like being able to read the menu. It does not mean you know what to order, whether the kitchen is closed, or why the waiter looks nervous.

For underwriting, the harder work is interpretation. A system needs to understand that “TIV,” “total insured value,” “building limit,” and “property values” may be related but not always interchangeable. It needs to know that a loss run valued as of last month is more useful than one from eight months ago. It needs to catch that a payroll figure in a workers’ compensation submission may not match the revenue trend in the financials.

That is where many platforms disappoint. They can read documents, but they cannot manage underwriting ambiguity.

The problem gets even bigger when files include legal or regulatory context from unfamiliar jurisdictions. A multinational account, for example, might include administrative sanctions, public-sector contract material, or local legal correspondence. If you want a sense of how specialized those documents can become in another market, a Colombian administrative-law practice such as Diana Ordoñez Abogada gives a useful example of the kind of local context that may sit behind a single attachment. Underwriting software should not pretend those documents are just generic PDFs.

Portals help, but they do not solve the broker reality

I like portals when they are well designed. I also like vegetables, but that does not mean I expect every broker to eat them at every meal.

Forcing every submission into a perfect portal sounds efficient until you see the abandonment rate, the duplicate emails, and the “Can I just send this to you?” messages. Brokers live under deadline pressure too. If your process makes it harder to submit business, someone else will happily accept the messy email.

That does not mean insurers should accept chaos forever. It means the software should meet the market where it is, then quietly improve the data underneath.

A practical underwriting platform should take in the messy file packet, extract what it can, flag what it cannot, and move the risk forward without requiring everyone outside your organization to change behavior overnight. Over time, you can improve broker guidance, templates, and submission quality. But you should not need a market-wide etiquette seminar before your automation works.

What good underwriting software should do with messy files

If I were testing underwriting software for insurance today, I would bring the ugliest submissions I could find. Not the nightmare account with 800 pages, necessarily. I would bring the normal ugly ones, because those are the files that quietly drain capacity every day.

A strong system should be able to ingest the whole packet, including email bodies and attachments. It should classify documents, pull the right fields, compare related values, preserve source evidence, and route exceptions without making the underwriter babysit every step.

It should also connect to external data sources when needed. If a property file includes an address, enrichment should be simple. If an auto submission includes drivers, vehicles, territories, or prior losses, the workflow should support the right checks. This is where pre-built API templates can matter, because enrichment that takes a six-month integration project is not exactly “automation.” It is a hobby with invoices.

Most importantly, the extracted data should not die inside the workflow. It should feed reporting and analytics. Otherwise, you automate individual tasks but still cannot answer portfolio-level questions like, “Where are referrals spiking?” or “Which brokers consistently submit incomplete schedules?” or “How do our renewal assumptions compare with the market?”

That is why I keep coming back to the data layer. If you want a deeper discussion of how poor data undermines underwriting decisions, our piece on what AI in insurance underwriting gets wrong without good data covers the issue from the decision-quality angle.

The real cost is not the extra five minutes

People underestimate the cost of messy files because they count the visible delay. Five minutes to rename a file. Ten minutes to re-key a schedule. Fifteen minutes to chase a missing loss run.

That is annoying, but it is not the full cost.

The bigger cost is uneven decision-making. One underwriter catches the discrepancy. Another misses it. One team validates every field manually. Another trusts the first attachment. One office has a spreadsheet workaround that no one else knows exists. Congratulations, you now have operational folklore.

Messy files also create leakage in more subtle ways. Slow quote turnaround can lose good risks. Manual errors can affect pricing. Weak audit trails can make referrals harder to defend. Poor data capture can leave portfolio managers guessing during renewals, reinsurance discussions, or capacity planning.

And when claims eventually arrive, the quality of the underwriting record matters. The FBI notes that insurance fraud remains a major cost to the industry, with non-health insurance fraud estimated at more than $40 billion per year in the United States. Clean, traceable underwriting data will not eliminate fraud, but it gives claims and fraud teams a better starting point than a folder full of mystery PDFs.

How I would test a vendor before signing

Here is my simple buying advice: do not let the vendor choose the files.

Bring your own submissions. Include broker emails, bad scans, mixed PDFs, spreadsheets with hidden tabs, missing fields, conflicting data, and duplicate versions. Then ask the vendor to process them live or as close to live as their security process allows.

I would test five things.

- Can it identify what each file is? The system should separate applications, schedules, loss runs, supplemental forms, statements of values, and supporting documents without constant manual sorting.

- Can it find conflicts instead of hiding them? If two documents disagree, the software should flag the issue and show the sources.

- Can an underwriter verify the answer quickly? Extracted data should link back to the exact document location, not vanish into a black box.

- Can it work with your existing systems? If the data has to be re-keyed after extraction, you have simply moved the bottleneck.

- Can it turn workflow data into management insight? If automation does not improve reporting, capacity planning, and portfolio visibility, you are leaving value on the table.

That last point is where many projects lose momentum. The underwriting team gets a faster task, but leadership still lacks clean operating data. Then everyone wonders why the transformation story feels thin.

Where Inaza fits

At Inaza, we think messy files are the starting point, not an exception to be handled later. The platform is built to support all file types, integrate with existing systems, and help insurers, MGAs, and brokers automate underwriting, claims, customer service, and operations without forcing teams through heavy retraining.

The workflow side matters, of course. Inaza includes customizable automation workflows and 250+ workflow templates, which helps teams move faster without getting stuck in endless proof-of-concept theatre. But the more interesting part, in my view, is what happens after the workflow runs.

Because Inaza has a unified data warehouse underneath, the data captured from messy files can feed reporting, analytics, and dashboards. That means the same automation that reduces admin work can also improve visibility into submissions, referrals, broker performance, and portfolio trends. With pre-built API templates for sources such as Verisk, LexisNexis, and HazardHub, workflows can also be enriched without turning every improvement into a custom integration slog.

For teams dealing with commercial lines admin overload, this connects directly to the broader problem we covered in Commercial Lines Underwriting Still Runs on Admin Work. The files may look like the problem, but the real issue is the operating model around them.

Frequently Asked Questions

Why does underwriting software for insurance fail on messy files? It usually fails because it was designed around clean data entry rather than real submission packets. Real files include mixed formats, duplicate versions, missing fields, contradictory values, email context, and supporting evidence. If the software cannot classify, extract, validate, and preserve source context, underwriters still end up doing the work manually.

Can OCR solve messy underwriting documents? OCR helps, but it is only one piece. Reading text from a file is not the same as understanding what the document is, whether the data is current, which source should be trusted, or where conflicts exist. Underwriting workflows need interpretation, validation, routing, and auditability.

Should insurers force brokers to use portals instead of email? Portals can improve consistency, but forcing every broker into a rigid process can create friction and quote abandonment. A better approach is to accept real-world submissions, automate extraction and validation behind the scenes, and gradually improve submission standards over time.

What file types should underwriting software handle? At minimum, it should handle PDFs, scanned documents, spreadsheets, images, email bodies, forms, loss runs, schedules, and supporting attachments. More importantly, it should understand the role each file plays in the underwriting decision.

How should insurers measure success with messy-file automation? Look beyond time saved per submission. Measure quote turnaround, referral quality, re-keying reduction, exception rates, broker completeness, audit trail strength, and the quality of portfolio reporting produced from the captured data.

Make the ugly files useful

Messy files are not going away. Brokers will still send odd attachments. Schedules will still arrive with missing columns. PDFs will still be scanned at strange angles by someone who appears to be fleeing the building.

The goal is not to make every file perfect before underwriting starts. The goal is to make the software resilient enough to handle reality.

If your underwriting team is spending more time cleaning files than assessing risk, it may be time to rethink the workflow underneath. Inaza helps insurers, MGAs, and brokers automate the messy operational work around underwriting and turn the data captured along the way into useful business intelligence.