What a Claim Database Should Tell You Before Reserves Move

I’ve sat in enough reserve reviews to know the most expensive sentence in claims is, “We didn’t see that coming.” Usually, we did see it coming. We just saw it in six different places: one adjuster note, one PDF invoice, one stale diary entry, one attorney email, one photo upload, and one payment transaction nobody tied together.

Here’s my hot take: if your claim database only tells you why reserves moved after the fact, it is not a database. It is a filing cabinet with better posture.

A useful claim database should warn you before reserves move. It should surface the claim facts, missing information, behavioral changes, litigation signals, and portfolio patterns that make a reserve change likely. Not to replace adjusters, because good adjusters are worth their weight in closed files, but to make sure they are not doing detective work with a flashlight and a spreadsheet.

Reserve changes rarely come out of nowhere

A reserve move is usually the official version of something that started earlier. The body shop sent a supplement. Treatment continued past the expected window. A claimant stopped responding and then returned with counsel. Rental days crept up. Liability shifted from “clear” to “hmm, let’s talk.” A demand package arrived with medical bills that did not match the accident facts.

When I was handling auto bodily injury files years ago, I had a claim that looked painfully ordinary at FNOL. Rear-end loss, soft tissue complaint, low speed, no airbag deployment. The first reserve was reasonable. Then came three chiropractic visits, then twelve, then MRI language started appearing in the notes, then the claimant attorneyed up. By the time reserves moved, the database had already been whispering for weeks. We just did not have one place where those whispers became a sentence.

That is the job of a modern claim database: turn weak signals into an early view of severity.

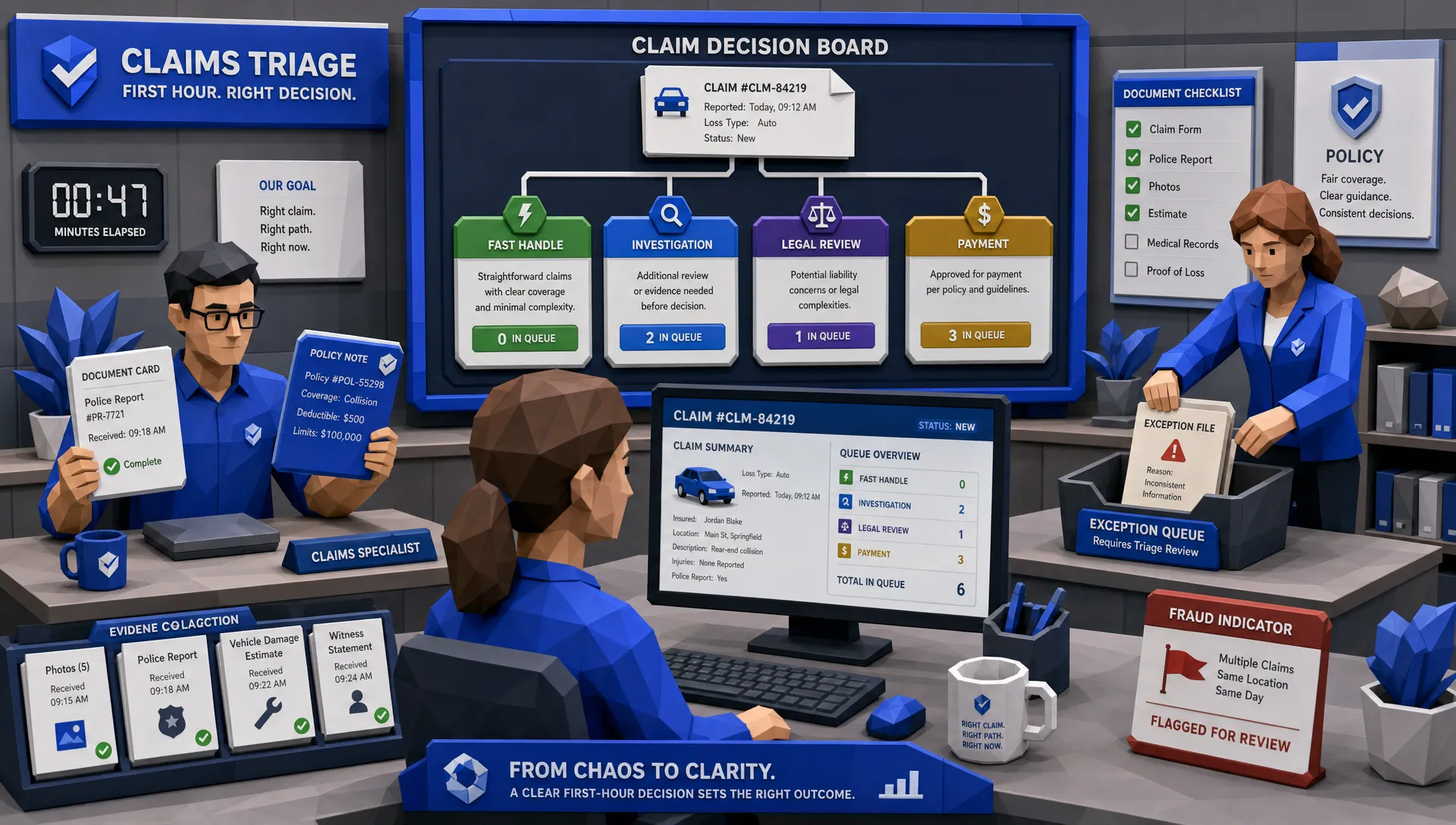

The first thing it should show: the claim story in sequence

Claims are stories with timestamps. Bad databases turn those stories into junk drawers.

Before reserves move, a claim database should show the complete timeline: FNOL, coverage checks, liability decisions, adjuster notes, payments, invoices, photos, police reports, medical records, attorney correspondence, repair supplements, diary changes, and customer communications. More importantly, it should show what changed and when.

The sequence matters. A $2,000 supplement two days after inspection is different from a $2,000 supplement after three weeks of parts delays and repeated shop contact. A claimant calling twice for status is different from a claimant going silent for a month and returning through counsel. Same data points, different story.

This is where many claim systems fall short. They store events, but they do not explain movement. A reserve-ready claim database should let a supervisor ask, “What changed since the last reserve review?” and get a clean answer without opening 19 tabs. If the answer requires coffee, a notepad, and mild profanity, the database is underperforming.

It should put missing information in financial context

Missing data is not just an administrative annoyance. It is often reserve volatility in disguise.

If liability is unclear, coverage is pending, medical records are incomplete, or repairability is unresolved, the database should not merely mark the item as “pending.” It should connect that gap to reserve uncertainty. A claim with an incomplete police report, conflicting statements, and early treatment should not sit in the same operational bucket as a claim waiting on a routine tow invoice.

The database should tell you which missing facts could change the economics of the file. For example, missing wage documentation in a bodily injury claim matters differently than a missing photo of a cracked bumper. A missing proof of repair might delay closure. A missing coverage exclusion review might change whether the claim should be paid at all.

I like to think of it the same way a homeowner thinks before repairing an appliance. If my refrigerator quits, I do not just ask, “Is there a repair ticket?” I want to know the likely repair cost, whether parts are available, and whether replacement makes more sense. Consumers can find that practical context in resources like Phoenix appliance repair tips and price guides. Claims teams deserve the same kind of grounded context inside the claim database: what is missing, why it matters, and how much it could change the outcome.

It should detect severity creep before it becomes obvious

Severity creep is sneaky. It does not always arrive with flashing lights. Sometimes it shows up as a slightly longer rental period, a second medical provider, a vague pain complaint that becomes a diagnostic test, or a repair estimate that suddenly includes structural work.

A strong claim database should flag the ingredients that historically lead to reserve increases. In auto physical damage, that might include supplement frequency, parts delays, rental duration, total-loss threshold proximity, storage fees, and vendor variance. In bodily injury, it might include attorney representation, treatment duration, diagnostic escalation, venue, prior injury indicators, policy-limit exposure, and medical billing patterns.

The point is not to panic every time a file gets a new document. The point is to distinguish normal development from abnormal drift. If 80 percent of similar claims close within a certain range, and this claim begins to behave like the 20 percent that do not, someone should know before the reserve worksheet catches up.

That also matters for customer experience. J.D. Power’s 2024 U.S. Auto Claims Satisfaction Study continues to emphasize how cycle time and communication shape claimant satisfaction. Reserve accuracy and service speed are connected. When the database spots friction early, teams can act earlier, communicate better, and avoid the awkward “we need more time” conversation that nobody enjoys.

It should compare the file to similar claims, not tribal memory

Every claims department has a few people with elephant memories. They remember the weird hail event from 2017, the venue that suddenly got plaintiff-friendly, and the repair shop that always seems to find “new damage” on day nine.

Those people are valuable. They should not be the database.

Before reserves move, a claim database should compare the file against similar historical claims. Not vaguely similar, but meaningfully similar: coverage type, jurisdiction, vehicle type, injury category, attorney involvement, repair path, vendor, weather event, policy limits, and claim age.

This is where the database earns its keep. It should answer questions like: How did similar claims develop? When did reserves usually move? What drove the movement? Did early attorney involvement double the likelihood of litigation? Did a certain repair pattern increase supplement frequency? Did claims from one territory close 20 days slower than the book average?

That is not theory. That is operational leverage.

It should separate fraud signals from ordinary weirdness

Claims are messy. Human behavior is messy. If every inconsistency becomes a fraud alert, adjusters tune out faster than a teenager hearing “clean your room.”

Still, fraud risk belongs in the reserve conversation because questionable claims can distort both payment and expense. The FBI notes that non-health insurance fraud costs more than $40 billion per year, and the pressure is not easing. Digital documents, edited images, synthetic identities, and organized activity have made the old “squint at the invoice” method look a little quaint.

A claim database should show fraud indicators in context. A late-reported claim may be innocent. A late-reported claim with mismatched metadata, prior similar losses, inconsistent damage photos, and a suspicious provider pattern deserves a different level of attention.

The best systems do not scream “fraud” every five minutes. They rank concern, explain the drivers, and route the file appropriately. That protects the insurer, but it also protects honest policyholders from unnecessary delays caused by sloppy false positives.

It should expose operational lag as a reserve risk

Here is an underrated reserve signal: delay.

A claim can become more expensive simply because it sat too long. Delayed coverage decisions invite frustration. Delayed liability decisions invite disputes. Delayed repair approvals create rental leakage. Delayed medical review gives a questionable treatment pattern time to harden into a demand.

A claim database should show where the claim is stuck and what that delay usually costs. If attorney-represented BI claims in a certain queue are aging faster than comparable files, that is not just a staffing metric. It is a reserve issue. If supplements from one vendor sit unreviewed longer than others, that is not just workflow trivia. It may be leakage.

This is one reason I’m fond of dashboards that connect claim activity to financial outcomes. Counting open tasks is fine. Showing which open tasks are likely to affect reserves is much better.

It should connect reserves to underwriting, pricing, and reinsurance

Claims teams often treat reserves as a claims-only matter. I get why. Claims owns the file, takes the calls, negotiates the settlement, and gets the Monday morning questions.

But reserve movement is also underwriting intelligence.

If reserves are moving because a certain class of business has higher-than-expected injury severity, underwriting needs to know. If property claims in a territory are developing differently because repair costs changed, pricing needs to know. If a portfolio narrative is being prepared for reinsurance, reserve development patterns matter a lot.

A claim database should not trap this information inside claim notes. It should make the data usable across the business. For MGAs, carriers, brokers, and reinsurers, the real value is not only claim handling efficiency. It is knowing whether the book is behaving the way everyone thought it would.

That is where a unified data warehouse becomes more than a technology choice. It becomes a business control.

What “good” looks like before reserves move

If I were designing the reserve review screen for a claims leader, I would want it to answer a few plain-English questions quickly.

What changed since the last review? Which facts are missing? How does this claim compare with similar claims? What reserve range does the historical pattern suggest? Which factors are pushing severity up or down? Is the current reserve outside the expected band? What action should happen next?

Notice what is missing from that list: “Please download four spreadsheets and ask Steve if he remembers a similar one from last quarter.” Steve may be brilliant, but Steve also goes on vacation.

A good claim database should support adjusters, supervisors, actuaries, and leadership with the same underlying truth. The adjuster needs file-level guidance. The supervisor needs exceptions. The claims executive needs trend visibility. Finance needs confidence in reserve adequacy. Underwriting needs feedback from actual loss experience.

Same data, different lens.

Where automation fits, without making everyone roll their eyes

I have seen automation projects fail because they promised magic and delivered another queue. Claims people do not need magic. They need fewer swivel-chair tasks and better timing.

For reserve management, automation is useful when it captures data cleanly, updates the claim record as new information arrives, enriches the file with relevant third-party sources, and turns all of that into usable reporting. The goal is not to make every reserve decision automatic. The goal is to make reserve-impacting facts visible while there is still time to act.

This is where Inaza is focused. Inaza’s insurance automation platform can help insurers, MGAs, and brokers capture data from claims workflows, integrate with existing systems, and store key information in a unified data warehouse. From there, teams can use dashboards and analytics to see patterns across underwriting, claims, customer service, and operations. Inaza also supports customizable workflows and pre-built API templates, which helps teams enrich automations without rebuilding the plumbing every time.

The practical win is simple: when claim data is captured as work happens, reserve conversations become less reactive. You are no longer asking, “Why did this move?” two weeks too late. You are asking, “What is likely to move next, and what should we do about it?”

For a deeper look at connected insurance data, Inaza has also covered how insurers can understand risk better with a connected-data platform.

The uncomfortable truth about old claim databases

Many legacy claim databases were built to record transactions, not anticipate development. They are good at telling you what was paid, what was reserved, and who touched the file. That is necessary, but it is not enough.

Before reserves move, your database should be opinionated in the best possible way. It should tell you which claims deserve attention, why they deserve it, and what comparable history suggests. It should make reserve movement explainable rather than surprising.

If the system cannot do that, people compensate. Adjusters keep side notes. Supervisors build spreadsheets. Finance asks for manual extracts. Underwriting waits for quarterly loss reviews. Reinsurance narratives become archaeology projects.

That is expensive, even when no one books it as an expense.

Frequently Asked Questions

What is a claim database in insurance? A claim database is a centralized source of claim information, including FNOL details, documents, notes, payments, reserves, vendor activity, communications, and related policy data. A strong database does more than store records. It helps teams identify trends, risks, missing information, and likely claim development.

How can a claim database help before reserves move? It can flag early reserve indicators such as severity creep, delayed tasks, attorney involvement, repair supplements, prolonged treatment, fraud indicators, and outcomes from similar historical claims. This gives claims leaders time to review, intervene, and set more accurate reserves.

Should reserve decisions be fully automated? Usually, no. Reserve decisions often require judgment, especially in complex bodily injury, litigated, catastrophe, or coverage-sensitive claims. Automation should organize the facts, surface patterns, and recommend attention points so experienced claims professionals can make better decisions faster.

What data should insurers track to improve reserve accuracy? Insurers should track claim timelines, payment history, open tasks, medical and repair development, attorney involvement, vendor behavior, jurisdiction, coverage issues, similar-claim outcomes, and operational delays. The key is connecting those fields to actual reserve movement over time.

Why does a unified data warehouse matter for claims reserves? A unified data warehouse helps insurers connect claim activity to underwriting, pricing, operations, and portfolio performance. That makes reserve trends easier to explain and helps leadership see whether claim development is isolated, systemic, or tied to a broader book issue.

See reserve signals before they become reserve surprises

Reserve movement should not feel like a plot twist. With the right claim database, insurers can spot the signals earlier, explain the drivers clearly, and act before small issues become expensive ones.

If you want to see how Inaza helps claims and underwriting teams automate data capture, connect workflows, and turn claim activity into usable intelligence, visit Inaza and explore what a more connected insurance operation can look like.