Insurance Industry Challenges No One Solves with More Hires

Hot take: most insurance industry challenges blamed on talent shortages are not talent problems. They are workflow plumbing problems. You can keep hiring intelligent people, then ask them to copy values from PDFs, chase missing attachments, reconcile five systems, and apologize for delays they did not create. That is not staffing. That is expensive theater.

I have spent a decade around carriers, MGAs, brokers, and claims teams. When a queue grows, someone inevitably says: can we add two more analysts? Sometimes yes. Cat response, a new program launch, or a renewal spike genuinely needs hands. But if each new hire inherits the same broken intake, siloed data, and manual checks, you have not solved the problem. You have given the bottleneck a bigger payroll.

My favorite example is painfully ordinary. A senior underwriter I worked with once spent most of a Tuesday comparing a fleet schedule in Excel to vehicle details in a PDF and then checking a third-party source for VIN mismatches. She was one of the sharpest risk minds in the building. For that day, she was effectively a very expensive copy-and-paste machine with better judgment than the job required.

Why the hiring reflex feels right

Insurance work is full of pressure. Submissions pile up. Attorney demands arrive late Friday. Claims photos need review. Brokers want an answer yesterday. Customers want status now, preferably before they have finished typing the question.

So yes, more people feels logical. Capacity is visible. A new adjuster or underwriting assistant can take files out of a queue. A contractor can help during surge season. An offshore team can clear a backlog. I am not anti-hiring. Good people are the reason insurance works at all.

But hiring is often used as a painkiller for an operational injury. It dulls the pain while the fracture remains.

McKinsey has written that underwriters can spend up to 60 percent of their time on administrative work instead of risk assessment in its article on automating the insurance industry. Anyone who has sat near an underwriting pod can confirm the vibe: smart people, mediocre tooling, too many re-keys.

The same pattern shows up in claims. A backlog is rarely just a lack of adjusters. It is missing information at FNOL, documents trapped in email, photos that need verification, inconsistent notes, and supervisors who cannot see where the process is stuck until everyone is already irritated.

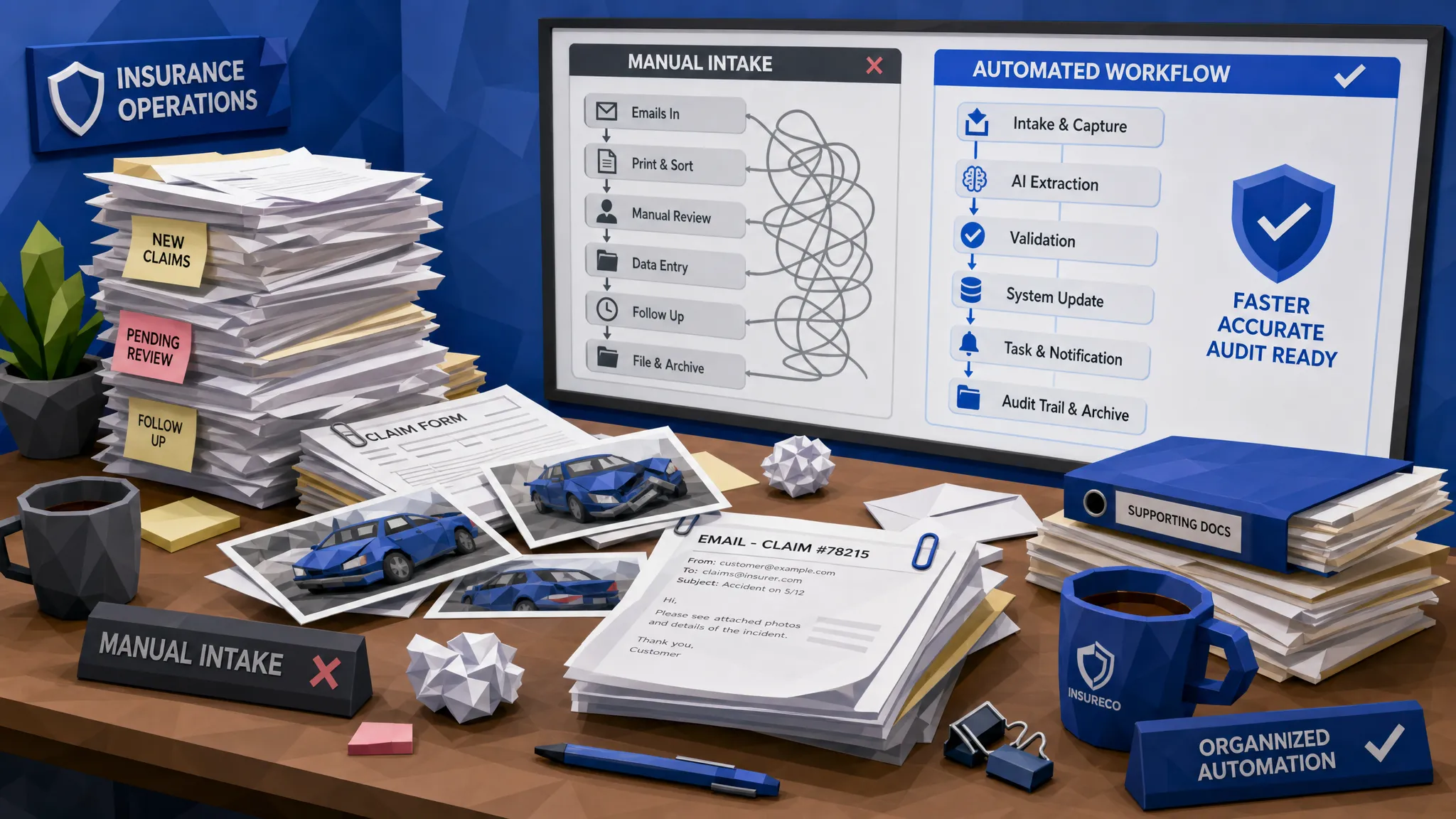

Challenge 1: messy intake is eating the industry

The first of the big insurance industry challenges is deceptively boring: work arrives messy.

Applications come in as PDFs, spreadsheets, scanned forms, broker emails, portals, handwritten notes, image files, loss runs, medical bills, demand packages, and occasionally the dreaded forwarded email chain with one useful attachment buried under seven signatures. If you are lucky, the file name contains something more helpful than final_final_v3.pdf.

No amount of hiring changes the fact that messy inputs create messy downstream decisions. More staff can read more documents, but they cannot magically make inconsistent data consistent.

For MGAs and carriers, the intake problem hits everywhere. Underwriting teams lose time structuring submissions. Claims teams lose time building complete claim packs. Fraud teams lose time hunting across systems for context. Customer service teams lose time answering status questions because the actual status is hidden inside someone else’s inbox.

Here is the uncomfortable bit: many organizations call this process expertise. I call it institutional memory doing unpaid overtime.

When a team relies on a few veteran employees who know where everything is, who to ask, and which spreadsheet is the real one, the business has a single point of failure wearing a headset.

Challenge 2: data lives everywhere except where decisions happen

In insurance, we love data. We buy it, enrich it, argue about it, and occasionally forget where we put it.

A policy admin system has one version of the customer. A claims system has another. The broker email has updated vehicle information. A third-party report has a critical risk signal. A spreadsheet has the latest manual override. Finance has numbers that operations will see next month.

Then leadership asks a perfectly reasonable question: why are turnaround times increasing on this book?

Cue the data scavenger hunt.

This is where more hires can actually make things worse. Every additional manual handoff creates another interpretation of the facts. One person codes a claim one way. Another uses a slightly different description. One underwriter stores the reason for a declination in a note field. Another writes it in an email. Six months later, you do not have business intelligence. You have folklore.

A connected data layer matters because workflow automation should leave behind usable evidence. The system should record the completed task and the facts around that task: what came in, what was extracted, what was checked, what failed, who approved it, and what happened next.

That is why I like the shift from isolated automation to a true operating data foundation. We have written more about this in our guide to connected insurance data platforms, because this is where many insurers quietly win or lose. If your workflows do not capture clean data as they run, your dashboards will always be late, partial, or suspiciously pretty.

Challenge 3: fraud has become too fast for manual review

Insurance fraud has always existed. What has changed is the speed, polish, and accessibility of it.

The FBI notes that non-health insurance fraud costs the U.S. more than $40 billion per year. That figure is painful enough before we account for the new generation of manipulated documents, staged losses, synthetic identities, altered images, and exaggerated injury claims.

Verisk’s 2025 fraud report found that 98 percent of carriers surveyed say AI contributes to digital fraud, while 55 percent of Gen Z respondents said they would consider using AI tools to create fake claims. I do not say that to be dramatic. I say it because I have seen adjusters waste hours debating whether an image looks off, only to find the real clue was in metadata or a mismatch against prior claim patterns.

Hiring more fraud analysts helps only if they are reviewing the right files. If every claim receives the same manual suspicion, good customers wait longer and analysts burn out. If suspicious claims are buried among routine ones, leakage becomes a line item nobody wants to explain at quarter end.

The fix is not to turn every claims desk into a crime lab. The fix is to screen earlier, bring the right signals together, and route only the meaningful exceptions to specialists.

Challenge 4: underwriting talent is being used like clerical bandwidth

I will happily die on this hill: one of the worst uses of underwriting talent is asking underwriters to become data janitors.

Underwriters should be thinking about risk quality, pricing adequacy, appetite, portfolio balance, broker relationships, and whether a submission makes sense in the real world. They should not be spending prime working hours extracting driver data from a spreadsheet, checking whether a proof-of-prior document is attached, or manually comparing an MVR to an application.

That is not because those tasks are unimportant. They are very important. That is precisely why they should be standardized.

Manual verification has a sneaky cost. It does not only slow quote turnaround. It introduces inconsistency. One underwriter may catch a mismatch. Another may miss it under pressure. A third may apply a rule differently because the guideline is buried in a PDF last updated during the Obama administration.

More hires multiply the variation unless the workflow itself is clear, measured, and repeatable.

For MGAs, this is especially dangerous. Growth often means more submissions, more delegated authority pressure, more bordereaux scrutiny, and tighter expectations from capacity providers. If your underwriting process scales only by adding people, your expense ratio will eventually start tapping you on the shoulder like a waiter who wants the table back.

Challenge 5: customers now compare insurers to everyone else

Policyholders do not benchmark their claim experience against another insurer’s internal operating model. They compare it with banking apps, food delivery, travel refunds, and healthcare benefits that explain coverage in plain English.

This is where the industry sometimes gets grumpy. We say insurance is complex. True. We say regulation matters. Also true. We say claims require investigation. Absolutely.

But customers still want fast answers, clear status, and fewer repeated questions. If a consumer can understand insurance-covered personal training online with eligibility, coaching, and next steps laid out plainly, they will not be charmed by a three-week wait to confirm whether their auto claim has all required documents.

A quick personal example: after a minor parking lot accident years ago, a friend asked me why his insurer needed him to re-enter the same vehicle details he had already provided on the phone. I started explaining system separation, claim setup, and verification. Halfway through, he gave me the look people reserve for printer errors and airport delays. He did not care. And honestly, he was right.

Customers do not need to understand our plumbing. They just need the shower to work.

More customer service reps can answer more calls. But if the answer is still: we are waiting on another department, the experience does not really improve. It just becomes a faster delivery of the same disappointment.

Challenge 6: compliance has outgrown spreadsheet control

The compliance burden in insurance is not going down. State requirements, audit demands, model governance, document retention, claims handling deadlines, privacy expectations, and delegated authority reporting all require proof.

Not vibes. Proof.

The problem is that manual processes often leave weak evidence. A decision may be sound, but the audit trail is scattered. The data source is unclear. The timestamp lives in one system. The approval happened in an email. The exception rationale is in a note field that only one person knows how to find.

When regulators, reinsurers, capacity providers, or internal audit teams ask what happened, a team should not need three days and a séance to reconstruct the answer.

Hiring compliance staff helps with interpretation and governance. It does not automatically create clean logs, consistent controls, or real-time reporting. That has to be designed into the workflow.

The real fix: redesign the work before expanding the team

Here is my hot take in its simplest form: hiring solves capacity, but insurance’s biggest operational problems are usually design problems.

Before adding five people to a queue, ask why the queue exists. Before creating a new review team, ask what data would let you triage better. Before building another dashboard, ask whether the underlying workflow captures trustworthy data in the first place.

The best operators I know are not trying to remove humans from insurance. They are trying to remove avoidable friction from human work.

A healthier operating model usually has a few common habits:

- Capture data once, at the point it enters the business.

- Validate key fields before the file moves downstream.

- Route work based on risk, complexity, and urgency.

- Escalate exceptions with context, not just a ticket number.

- Measure cycle time, leakage, error rates, and rework in near real time.

Notice what is not on that list: ask Karen if she remembers where the prior version of the spreadsheet is saved.

What this looks like in underwriting and claims

In underwriting, better workflow design starts with intake. Submissions should be classified, key fields should be extracted, third-party checks should run where appropriate, and missing information should be flagged before an underwriter opens the file. If the risk is simple and within appetite, it should move quickly. If it is complex, the underwriter should see the reasons immediately.

In claims, the same logic applies. FNOL data should be captured cleanly. Images, invoices, police reports, medical documents, and attorney demands should be organized into a usable claim view. Fraud signals should appear early. Routine claims should not sit behind complex ones just because they arrived in the same inbox.

In customer service, the agent or automated response should not be guessing. It should know policy status, claim status, pending requirements, and the right next action. If the conversation is sensitive, such as injury, coverage denial, or suspected fraud, a human should step in with full context.

The theme is simple: stop making people assemble the truth from fragments.

Where Inaza fits into this conversation

Inaza was built around the idea that insurance teams should not need a yearlong transformation program to fix one broken workflow.

The platform supports automation across underwriting, claims, customer service, and operations. It integrates with existing systems, supports all file types, and includes 250+ workflow templates that can be customized for real insurance processes. In practical terms, that means teams can automate data capture, routing, reporting, and analytics without forcing everyone to relearn their jobs from scratch.

Inaza can also help teams deploy production-ready workflows quickly, in some cases from a single working session, rather than dragging everyone through endless proof-of-concept loops. For busy insurance teams, that time-to-value matters.

The part I care about most is the data warehouse underneath the workflows. Automation that only moves a file from A to B is useful. Automation that also captures the operational data behind every step is far more valuable. That is how leaders get better visibility into bottlenecks, leakage, turnaround times, workload mix, and portfolio trends.

Inaza also has pre-built API templates for data enrichment sources such as Verisk, LexisNexis, HazardHub, and others. That matters because insurance decisions are rarely based on one internal field. Risk and claims context usually come from multiple places, and the workflow should bring those signals together rather than making staff jump between tabs like they are playing a very dull piano.

For carriers, MGAs, and brokers trying to benchmark performance, Inaza’s use of industry benchmarks can also help teams compare against market references and build stronger narratives for portfolio reviews, reinsurance discussions, and renewals. That is the kind of operational intelligence you do not get by throwing more people at an inbox.

Where hiring still matters

I do not want this to read like a love letter to software at the expense of people. Insurance still needs experienced underwriters, adjusters, fraud investigators, compliance leads, and service teams. In fact, automation makes their expertise more important because it clears away the low-value work that hides the hard decisions.

Humans should own judgment. Humans should handle empathy. Humans should negotiate difficult claims, interpret gray areas, manage broker relationships, and make risk appetite decisions that require context.

But humans should not be the glue holding disconnected systems together. Glue is cheap. Experienced insurance professionals are not.

A practical test before your next hiring request

The next time a department asks for more headcount, try this exercise first.

Pick one queue that is causing pain. It might be new business submissions, proof-of-prior checks, claims intake, attorney demand review, invoice verification, or broker emails. Then pull ten recent files and trace every handoff from arrival to completion.

Do not ask how the process is supposed to work. Ask how it actually worked.

How many times was the same data entered? How many systems did someone check? Where did the file wait? Which decision required human judgment, and which decision required only cleaner information? How much of the delay came from missing data? How much came from unclear ownership?

This exercise is humbling. It also reveals whether you need more staff, better workflow design, or both.

In my experience, the answer is often both, but in the opposite order people expect. Fix the workflow first. Then hire for judgment, relationships, and growth, not for manual cleanup.

The bottom line on insurance industry challenges

The insurance industry challenges that matter most in 2026 are not mysterious. They are hiding in plain sight: messy intake, fragmented data, slow claims, fraud pressure, underwriting admin, compliance evidence, and customer impatience.

The uncomfortable truth is that many insurers have already hired around these problems for years. They have built heroic teams that keep the machine running through effort, memory, and caffeine. I respect that. I have been in those rooms. I have also seen what happens when one key person goes on vacation and suddenly the process looks less like an operation and more like a treasure hunt.

More hires can help when the work is truly growing. But if the work is broken, more hires just scale the breakage.

The winners will be the insurers that treat automation as operational plumbing, not a shiny side project. They will capture clean data at intake, connect workflows across departments, enrich decisions with external signals, and give their people the context they need to do higher-value work.

That is how you solve insurance industry challenges without turning every budget meeting into a headcount negotiation.

Frequently Asked Questions

What are the biggest insurance industry challenges today? The biggest challenges include fragmented data, slow manual workflows, fraud pressure, underwriting admin, claims delays, compliance demands, and rising customer expectations. Most are process and data issues rather than pure staffing shortages.

Can hiring more people solve insurance operations problems? Hiring helps when there is genuine volume growth or a need for specialized expertise. It does not fix poor intake, disconnected systems, inconsistent data, or unclear workflows. In those cases, more hires often make the process more expensive without making it better.

Where should insurers automate first? Start with high-volume, rules-heavy workflows where data is repeatedly entered or checked. Common starting points include submission intake, FNOL, document classification, proof-of-prior checks, invoice review, broker emails, and attorney demand triage.

Does automation replace underwriters and adjusters? No. Good automation should remove repetitive admin so underwriters, adjusters, and fraud specialists can focus on judgment, negotiation, customer conversations, and complex exceptions.

How should insurers measure whether automation is working? Track cycle time, touch time, rework, error rates, leakage, straight-through processing rates, customer satisfaction, and audit completeness. The key is to measure before and after, not rely on anecdotes.

Ready to fix the work, not just staff the backlog?

If your team is hiring around the same bottlenecks every quarter, it may be time to look at the workflow underneath. Inaza helps insurers, MGAs, and brokers automate underwriting, claims, customer service, and operations while capturing the data needed for real visibility.

Request a demo to see how production-ready workflows, data enrichment, dashboards, and insurance-specific automation templates can help your team move faster without adding another layer of manual work.