How Workers Comp Underwriting Automation Cuts Quote Delays

Ask a workers comp underwriter what slows down a quote and you will rarely hear: the risk was too complex. More often, you will hear something like: the payroll was split across three spreadsheets, the loss runs came in sideways, the broker email said same as expiring, and nobody could confirm whether the delivery drivers were employees or contractors.

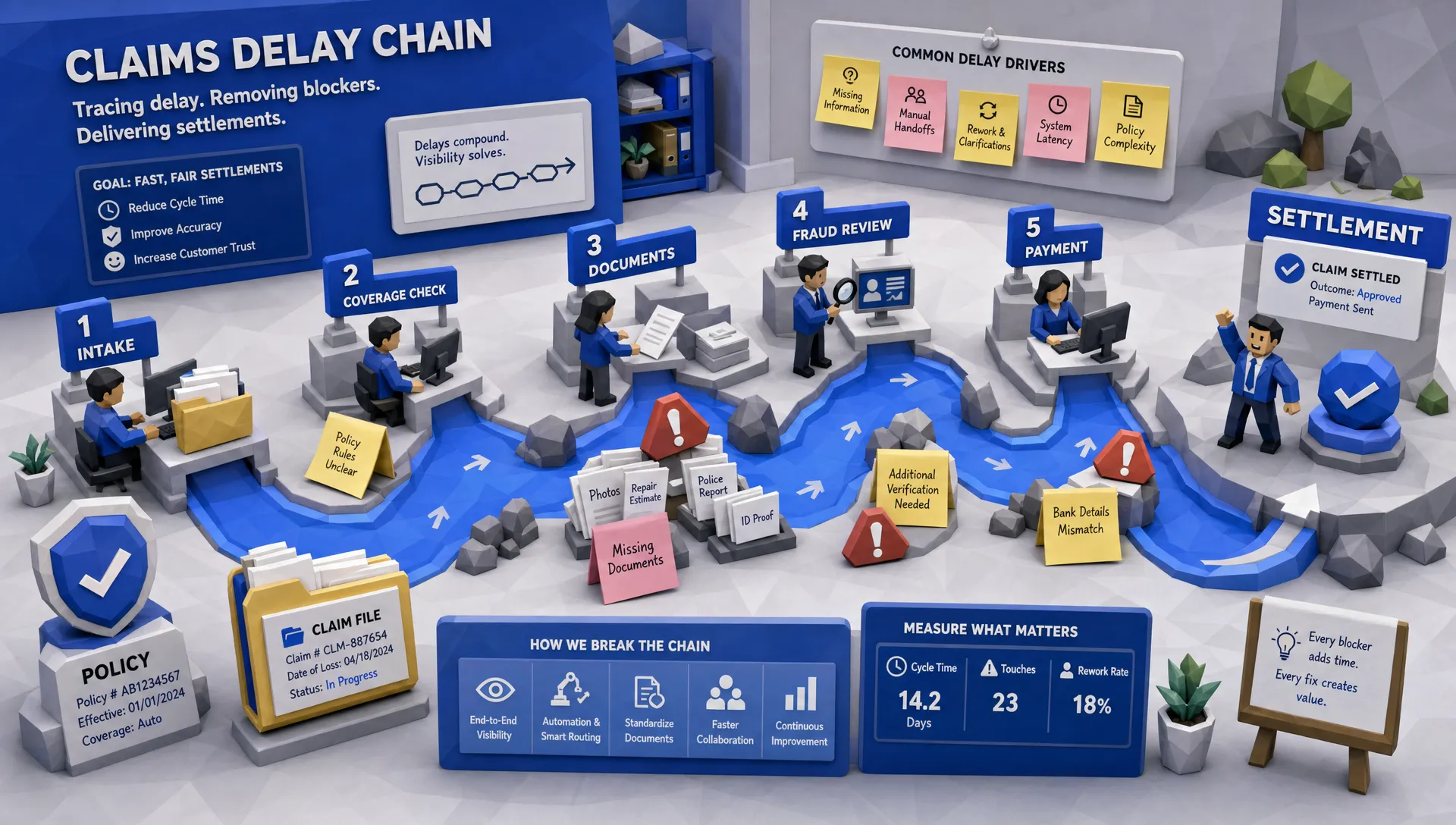

That is the boring truth. Quote delays usually do not start in risk judgment. They start in intake.

Here is my hot take after a decade around insurance operations: workers comp underwriting automation cuts quote delays fastest when it is aimed at the unglamorous work before rating begins. The winners are not always the carriers with the fanciest pricing model. They are the ones that stop making underwriters hunt for payroll, class codes, experience mod details, loss history, entity names, state exposures, and missing documents like they are in an office-themed escape room.

The real reason workers comp quotes get stuck

Workers compensation underwriting is detail-heavy by design. Payroll drives premium. Class codes drive rates. Loss history changes appetite and pricing. State rules matter. Ownership, operations, subcontractor exposure, safety practices, and prior coverage can all change the answer.

Now put that complexity inside a broker submission that arrives as one email, five attachments, one scanned PDF, and a spreadsheet named FINAL_v7_reallyfinal.xlsx. That is where delay lives.

I once watched an underwriter spend nearly 40 minutes on a contractor submission just trying to separate office payroll from field payroll. The risk itself was not wild. No explosives, no circus animals, no surprise roofing operation hiding in the back. The quote was delayed because the data was messy, and the underwriter had to act like a forensic accountant before doing any underwriting.

That is not a one-off pain point. McKinsey has estimated that underwriters can spend about 60 percent of their time on administrative work rather than risk assessment. In workers comp, that number feels painfully believable. When experienced underwriters spend their mornings re-keying payroll and chasing missing loss runs, quote speed suffers and so does morale.

The problem is not that underwriters dislike work. Underwriters love work when it involves judgment. They tend to dislike digital archaeology.

Why workers comp is uniquely allergic to bad data

Workers comp looks simple from a distance: payroll multiplied by rate, adjusted by experience and underwriting judgment. Easy enough, right? That is like saying a restaurant is simple because food goes on a plate.

A small business can have several very different exposures under one roof. A pizza shop may have counter staff, kitchen employees, delivery drivers, and a part-time bookkeeper. A construction firm may have clerical staff, project managers, field labor, subcontractors, and seasonal swings. If the submission lumps those payrolls together, the underwriter either has to pause and ask questions or make assumptions. Neither is great for speed.

The stakes are not theoretical. The U.S. Bureau of Labor Statistics tracks millions of workplace injury and illness cases each year, and workers comp exists because workplace exposure varies dramatically by role, industry, location, and operational behavior. A clean quote requires a clean picture of that exposure.

Automation helps because it turns a submission from a pile of artifacts into a usable underwriting file. It does not make the judgment for the underwriter in complex cases. It gets the file ready so the underwriter can actually judge.

How automation cuts quote delays where they actually happen

The phrase workers comp underwriting automation can sound bigger than it needs to. In practice, the best automation starts with a simple question: what makes this quote wait?

Usually, the answer is one of six things.

It turns every submission into structured data

A good workers comp submission may include ACORD forms, payroll schedules, loss runs, experience mod worksheets, supplemental applications, emails, PDFs, images, and broker notes. A bad one includes the same things, just with less mercy.

Automation can read and organize those inputs, then extract the core fields underwriters need: legal entity, FEIN, states of operation, payroll by class, number of employees, prior carrier, policy dates, open claims, paid losses, reserves, and other relevant details. The key is that the underwriter should not have to copy data from page 11 of a PDF into field 47 of a policy system.

That one change alone removes hours from busy submission queues. More importantly, it reduces the number of small errors that quietly create rework later.

If this sounds familiar, it is the same data quality issue we see across underwriting. I wrote about the broader problem in underwriting without good data is just guessing, and workers comp is a prime example.

It spots missing information before the file sits in someone’s queue

The old workflow is painfully familiar. A broker sends a submission. It waits. An assistant opens it. It waits. An underwriter reviews it. Then someone realizes the loss runs are missing or the payroll does not tie to the application. The broker gets an email two days later asking for clarification.

That is not underwriting. That is slow-motion ping-pong.

Automation can check completeness as soon as the submission arrives. If the file lacks three years of loss runs, the workflow can ask for them immediately. If payroll is missing for one state, it can flag the gap. If the experience mod is referenced but not attached, it can create a broker follow-up before the underwriter opens the account.

The difference is subtle but powerful. Instead of discovering problems after the file has aged, the system pushes the submission toward completeness from minute one.

It standardizes payroll and class code review

Class code and payroll review is where workers comp gets spicy. A business description may say light manufacturing, but the payroll detail may suggest warehousing, delivery, installation, or clerical exposure. A broker may use a prior class code that made sense three years ago but no longer fits after the insured added a new operation.

Automation can compare business descriptions, payroll splits, prior policy data, and class code patterns to flag mismatches. It can also highlight unusual payroll movements, such as a sudden drop in field payroll or a new state exposure with no corresponding explanation.

The underwriter still makes the call. That part matters. The system should not quietly force a class decision on a complex risk. What it should do is point to the exact place where the underwriter needs to look.

Think of it like a prep cook in a good kitchen. The chef still cooks, but nobody asks the chef to peel 40 pounds of potatoes before service.

It enriches the file without sending underwriters to ten different tabs

Workers comp underwriting often needs outside data. Business identity, locations, industry classifications, prior coverage, entity relationships, property characteristics, and other signals may all matter depending on the book.

When enrichment is manual, underwriters open separate systems, run searches, compare outputs, copy results, and hope they did not miss anything. That creates delay and inconsistency. One underwriter may check one source. Another may check three. A newer underwriter may not know which source to trust.

Automation can bring that enrichment into the workflow through pre-built API connections and controlled rules. For example, a team may want to validate business identity, confirm location data, enrich industry details, or surface third-party risk signals before the quote moves forward. When the data appears in the same underwriting flow, decision time drops.

Clean entity data deserves special mention. If an insured has multiple entities, new subsidiaries, or overseas structures, legal names and ownership details can make the difference between a clean quote and a compliance headache. The same principle applies in corporate structuring, where UAE company setup and compliance advisers help businesses keep entity records clear and usable. In workers comp underwriting, sloppy entity data can mean the wrong employer, wrong state, or wrong coverage assumptions.

It routes the easy, the messy, and the impossible differently

Every submission does not deserve the same treatment. That may sound obvious, but many underwriting teams still run simple renewals, incomplete new business, out-of-appetite accounts, and complex multi-state risks through the same queue.

That is how delays pile up.

Automation can triage. A straightforward renewal with clean payroll, expected loss history, and no appetite issues can move quickly. A submission missing key documents can go back for completion. A risk outside appetite can be declined faster and more politely. A complex account can be routed to a senior underwriter with the right context already attached.

This is where quote speed improves without lowering underwriting standards. You are not telling underwriters to spend less time on serious risk. You are making sure they do not spend serious time on unserious admin.

It creates a record of what happened

This part is less flashy, but underwriters and managers learn to love it.

When automation captures the data flowing through the quote process, leaders can see where delays actually occur. Is the broker taking three days to respond? Are loss runs the main blocker? Are certain states slower? Are new ventures creating referral spikes? Are class code discrepancies common in one segment?

Without that visibility, quote delay becomes a vibe. And vibes make terrible operations dashboards.

A unified data warehouse changes that. Instead of only automating today’s task, the insurer builds a record of submissions, exceptions, decisions, follow-ups, and outcomes. That makes it much easier to improve workflows, coach teams, and explain operational performance to leadership.

The broker experience improves before the expense ratio does

When we talk about automation, insurance teams often jump straight to expense savings. Fair enough. Everyone has a budget, and nobody gets a trophy for having the most manual process.

But the first visible win is often broker experience.

Brokers do not need every quote instantly. They do need clarity. If the answer is yes, tell them quickly. If the answer is no, tell them quickly. If the answer is maybe, tell them exactly what is missing.

I have seen brokers forgive a tougher price faster than they forgive silence. Silence makes them assume the submission fell into a black hole. And once a broker believes your inbox is a black hole, you do not get their best submissions first.

Workers comp underwriting automation helps by turning broker communication into a controlled process. Instead of generic requests like please send complete submission, the broker receives specific follow-ups: missing payroll by state, loss runs for 2022 to 2024, clarification on subcontractor certificates, or confirmation of employee count. Specificity saves everybody’s time.

What to automate first if your goal is faster quotes

If you want quote delays down quickly, do not start by trying to automate the hardest underwriting judgment in your book. Start earlier.

Begin with submission intake. Can the system read the broker email and attachments, identify the line of business, create a file, and extract core fields? Then move to completeness checks. Can it tell whether required documents are missing before an underwriter reviews the file? Next, automate payroll normalization and loss run extraction. Then add enrichment and referral routing.

Pricing automation may come later. In my experience, the fastest operational wins happen before rating. A clean submission with clear data moves faster even if the final pricing decision still belongs to a human underwriter.

That is the practical path. Cut the waiting. Cut the re-keying. Cut the vague broker follow-ups. Then improve decisioning.

What good looks like in the metrics

If you are implementing automation, measure quote delay in pieces. The total submission-to-quote time matters, but it hides too much.

Track submission received to first review, first review to complete file, complete file to quote, and quote to bind. Watch the percentage of submissions that arrive complete, the number of broker follow-ups per quote, re-keying hours, referral rates, decline turnaround time, and error corrections after quote. If you can track these by broker, class, state, and underwriter team, you will quickly see where the real bottlenecks live.

The goal is not to make every account straight-through. Workers comp has too many legitimate exceptions for that fantasy. The goal is to make simple work fast, messy work visible, and complex work worth the underwriter’s time.

The biggest implementation mistake: automating around bad habits

Here is where I risk annoying a few people. Automation will not rescue a broken underwriting process if nobody is willing to define what good looks like.

If every underwriter asks for different documents, if appetite rules live in someone’s memory, if class code guidance is buried in old emails, or if management cannot agree on referral thresholds, automation will simply expose the chaos faster.

That is not a reason to avoid it. It is a reason to use implementation as a cleanup exercise. Define the minimum submission requirements. Standardize the questions. Agree on what gets referred. Decide which data sources are authoritative. Write down the exceptions.

The best automation projects are part technology, part operational discipline, and part group therapy. I say that lovingly.

How Inaza helps cut workers comp quote delays

Inaza’s insurance automation platform is built for exactly this kind of workflow problem. It helps insurers, MGAs, and brokers automate data capture, underwriting workflows, reporting, and analytics while integrating with existing systems.

For workers comp teams, that means submissions can be ingested from different file types, structured into usable data, enriched through integrations, checked against configurable workflow rules, and routed based on the way the business actually underwrites. Inaza also has a unified data warehouse underpinning the automation, so teams can move beyond faster processing and see where quote delays, exceptions, and leakage are coming from.

That last point is important. Workflow automation is useful. Workflow automation plus business intelligence is where leadership gets leverage.

Inaza offers 250+ workflow templates, customizable automations, support for all file types, and pre-built API templates. It is designed to work with existing systems, which matters because most insurers are not looking for a core replacement project just to fix quote delays. And yes, avoiding six months of proof-of-concept theater is good for everyone’s blood pressure.

Frequently Asked Questions

What is workers comp underwriting automation? Workers comp underwriting automation uses software workflows to capture submission data, validate required information, enrich files, route exceptions, and reduce manual work during quote preparation. The underwriter still owns judgment on complex risks.

How does automation reduce workers comp quote delays? It cuts delays by extracting data from submissions, flagging missing documents immediately, standardizing payroll and class code review, automating broker follow-ups, and routing accounts based on appetite and complexity.

Does automation replace workers comp underwriters? No. The best use of automation is to remove administrative work so underwriters can focus on exposure analysis, pricing judgment, broker negotiation, and complex referrals.

What should insurers automate first in workers comp underwriting? Start with submission intake, document extraction, completeness checks, payroll normalization, loss run review, and broker follow-up workflows. These steps usually create faster ROI than trying to automate every pricing decision on day one.

Can underwriting automation work with legacy insurance systems? Yes, if the platform is designed for integration. The practical approach is to connect automation to existing policy, rating, CRM, email, and data systems rather than forcing a full replacement project.

Ready to cut quote delays?

If your workers comp team is still waiting on missing payroll files, re-keying loss runs, or sending the same broker follow-up for the hundredth time, the issue is not effort. It is workflow design.

Inaza helps insurance teams automate underwriting operations without ripping out existing systems. If you want faster quotes, cleaner data, and better visibility into where submissions slow down, we should talk.