Business Intelligence in Insurance That Teams Actually Use

Here is my hot take: most BI in insurance is built for board packs, not for the people who decide whether money enters or leaves the building.

I have seen beautiful dashboards with every shade of blue known to consulting. They had filters, drilldowns, and a logo in the top right. They also had the life expectancy of a gas station sandwich. The launch meeting was enthusiastic. Two weeks later, the underwriting team was back in Excel, the claims team was back in email, and someone in operations was manually stitching together a weekly report at 7 p.m. on a Thursday.

Business intelligence in insurance only works when it fits how teams actually work. Underwriters do not want a museum of charts. Claims adjusters do not want to click through six screens to find out what changed. Fraud analysts do not need more noise. They need trusted signals, in context, at the exact point where a decision has to be made.

That sounds obvious. In practice, it is where many insurers trip over their own data laces.

The problem with dashboard-first BI

Insurance companies are not short on data. We have policy data, claims data, broker data, documents, emails, call notes, adjuster notes, loss runs, MVRs, VINs, property data, payment data, litigation data, and enough spreadsheets to qualify as a separate ecosystem.

The problem is that too much of it arrives late, lives in silos, or gets cleaned up only after the operational moment has passed. If a report tells you last month that a quote queue was clogged, that is interesting. If it tells the underwriter right now that three submissions are missing the same data point and one broker is repeatedly causing rework, that is useful.

There is a big difference.

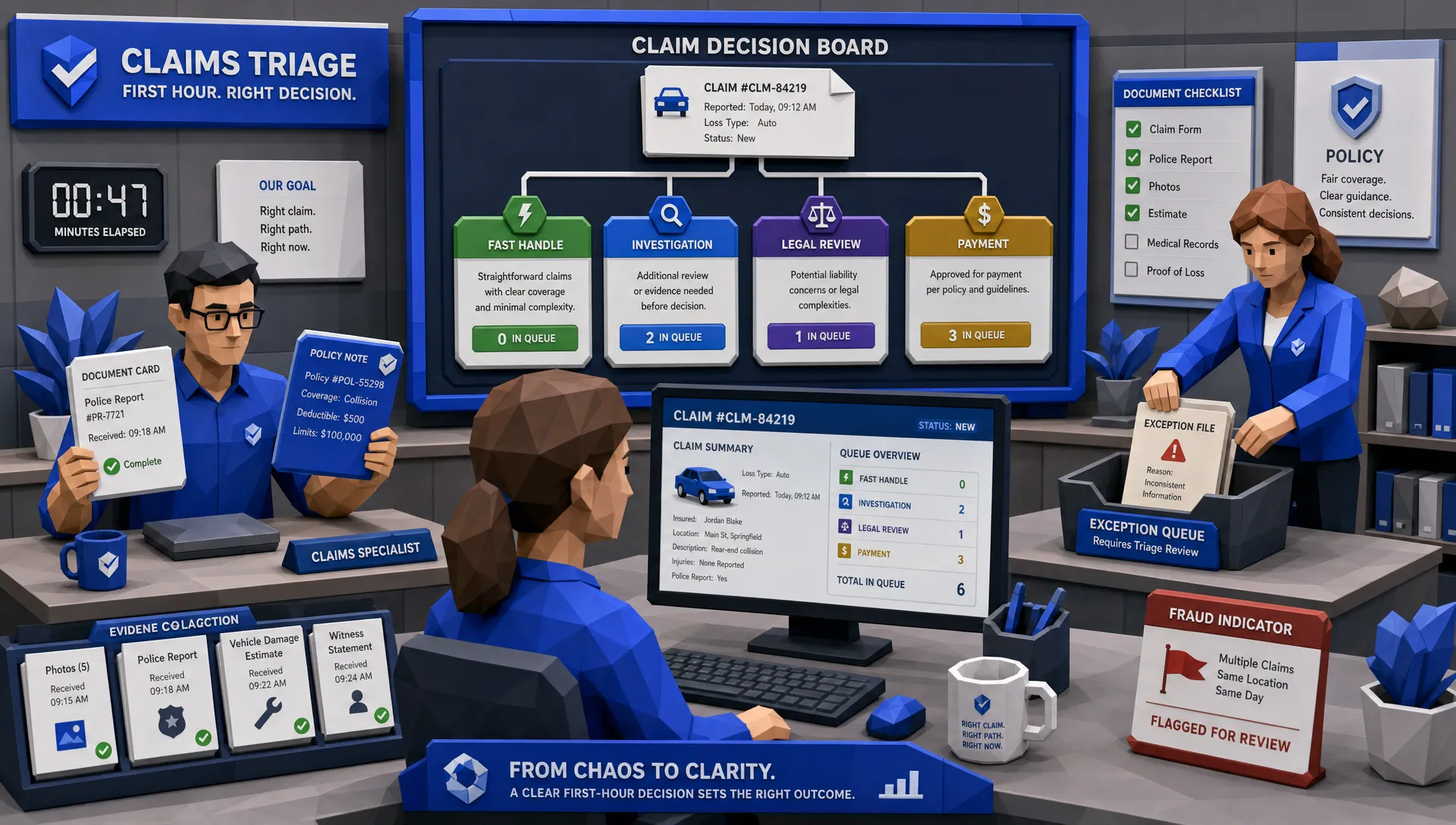

I once sat with a commercial auto underwriter who had thirteen tabs open. Thirteen. One core system, two spreadsheets, three email threads, a rating tool, a loss run PDF, a vehicle lookup, a broker portal, and a sticky note that had somehow become critical infrastructure. When I asked what BI would help, she did not ask for a new dashboard. She said, I just want to know which submission is safe to move and which one is going to bite me later.

That is the standard. If your BI cannot help with that kind of decision, it is probably decoration.

What business intelligence in insurance should actually do

Good BI starts with decisions, not charts.

For an insurer, MGA, broker, reinsurer, or claims organization, BI should answer questions that sit close to revenue, leakage, service, and risk. It should show where work is slowing down, where decisions are inconsistent, where premium is leaking, where claims are escalating, and where a portfolio is drifting away from plan.

A useful BI view should help someone answer questions like these in under 30 seconds:

- Which submissions should be handled first because they are complete, profitable, and time-sensitive?

- Which claims look routine, and which ones need early specialist attention?

- Which brokers or agents are driving avoidable rework?

- Which underwriting rules are creating too many exceptions?

- Which segments are performing differently from expectations?

If the answer requires a data analyst, a Slack thread, and three exports, it is not business intelligence. It is a treasure hunt.

McKinsey has estimated that underwriters can spend up to 60% of their time on administrative work. That number has always bothered me because underwriters are not hired to chase missing fields. Adjusters are not hired to copy dates between systems. Fraud analysts are not hired to review false positives all afternoon. BI should reduce that drag, not add another window to check.

Start with the workflow, not the warehouse

Data warehouses matter. I am not here to start a fight with the data team. They have enough trauma from field naming conventions already.

But a warehouse on its own does not create adoption. The winning move is to connect BI to workflows. When underwriting intake, claims triage, attorney demand review, customer service, and fraud checks all generate clean operational data as work happens, BI becomes a byproduct of the business, not an after-hours reporting exercise.

This is where insurance has an advantage over many industries. Our processes are full of meaningful events. A submission arrives. A document is missing. A risk gets enriched. A rule fires. A quote is referred. A claim moves from FNOL to investigation. A demand letter is received. A reserve changes. A fraud flag is cleared. Each of those events tells a story.

The trouble is that many systems only store the final chapter. Bound or not bound. Paid or denied. Open or closed. That is not enough.

The operational story in the middle is where the gold lives. Which step took too long? Which data source reduced rework? Which rule caused unnecessary referrals? Which adjuster team is handling complex claims faster without increasing leakage? Those are the questions that move combined ratio, expense ratio, and customer satisfaction.

If you want a deeper view of this idea, Inaza has written about building a connected insurance data platform that links the work itself to the data insurers use to make decisions.

The data most BI projects miss

Traditional insurance BI tends to focus on outcomes. Premium written. Loss ratio. Claim count. Average severity. Quote volume. Bind rate. These are necessary, but they are lagging indicators. They tell you where you landed after the plane has already touched down, nicely or otherwise.

Teams also need process intelligence. That means timestamps, handoffs, exception reasons, missing data patterns, referral causes, document types, communication delays, enrichment results, and audit trails.

I like to call this the operational exhaust of insurance. It may not sound glamorous, but it tells you how the machine is running. When captured properly, it shows whether the issue is pricing, appetite, staffing, data quality, broker behavior, fraud pressure, or simply a workflow designed by someone who has never processed a renewal in their life.

In claims, this matters even more. J.D. Power's 2024 U.S. Auto Claims Satisfaction Study highlighted how settlement timelines still weigh heavily on customer satisfaction. If a carrier only looks at average cycle time after month-end, it misses the chance to intervene when a claim is stuck on day three because a document was unreadable or a liability note was incomplete.

That is the difference between reporting and operating.

BI that teams trust is boring in the best way

The most useful BI usually looks less exciting than the vendor demo. That is a compliment.

Teams adopt BI when they trust the numbers. Trust comes from plain definitions, consistent inputs, and visible lineage. If one dashboard says bind rate is 19% and another says 24%, the business will not debate methodology for long. They will ignore both and go back to the spreadsheet called Final_v7_ACTUAL_FINAL.xlsx.

We have all seen that file. It is never final.

Trust also means showing why a metric changed. If quote turnaround improved, was it because the team got faster, the submission mix got easier, a new intake workflow reduced re-keying, or a major broker sent fewer messy files? If claims severity rose, was it medical inflation, attorney involvement, venue mix, fraud patterns, or delayed triage?

Good BI does not just display movement. It explains enough context for a manager to act without calling a committee meeting.

This is also why auditability matters. Insurance is a regulated business. A pretty chart that cannot be traced back to the underlying events is risky. A BI layer built from workflow events, with timestamps and decision records, is far more defensible. It supports management reporting, compliance review, operational coaching, and the occasional uncomfortable conversation with finance.

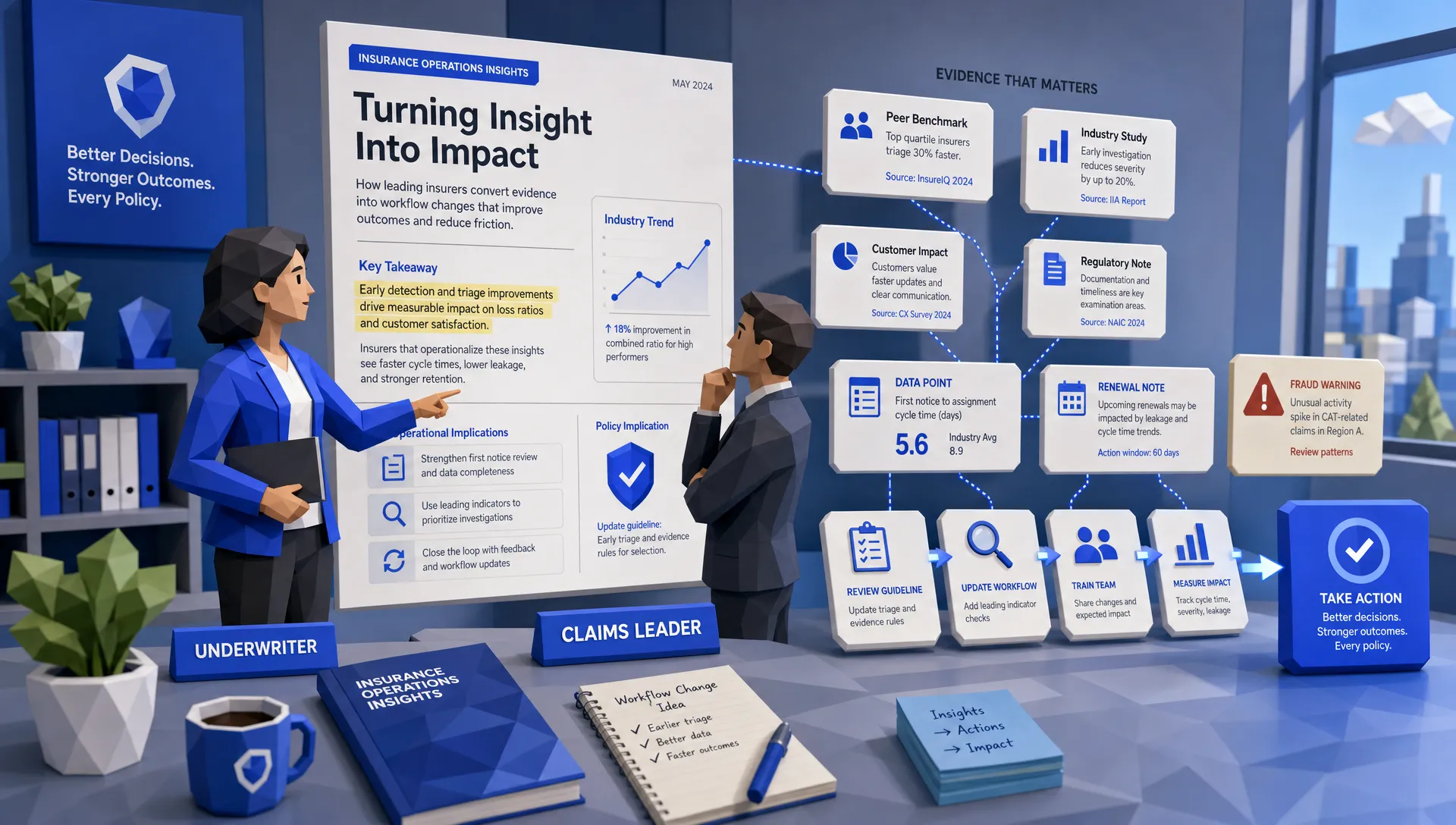

Benchmarks turn BI from internal reporting into strategy

Here is another hot take: internal trends are useful, but they can be dangerously flattering.

If your quote turnaround improved from eight days to six, that sounds great until you learn the market is at two. If your loss ratio is improving, that may be excellent, or it may simply mean the whole segment improved and you are still underperforming peers. Context matters.

That is why benchmarks are one of the most underrated parts of business intelligence in insurance. They help teams understand whether performance is genuinely strong or merely less bad than last quarter. There is a difference, though both may earn applause in the wrong meeting.

For MGAs and carriers, benchmarks can help with portfolio steering, renewal strategy, reinsurance conversations, capacity discussions, and board reporting. For reinsurance brokers, they can support a clearer narrative around a portfolio. For underwriters, they can show where appetite and pricing are drifting from market reality.

Inaza supports industry benchmarks such as Aon, Munich Re, Howden, and others within its system, based on the context provided by the business. The practical value is simple: a team can compare internal performance against market reference points instead of arguing in a vacuum.

A loss ratio chart without context is a weather report that only tells you it is raining on your own driveway.

Put the insight where the work happens

The best BI adoption trick is not a training session. It is placement.

Put the insight in the underwriting queue. Put the claim signal in the adjuster workflow. Put the fraud indicator beside the evidence. Put the broker performance trend inside the operations review. Put the portfolio benchmark in the renewal preparation pack.

Do not make people go looking for intelligence. The workday is already full of interruptions, and nobody wakes up excited to log into a separate analytics portal before coffee.

This is why workflow automation and BI belong together. When a workflow captures data and displays the right signal back to the user, adoption becomes natural. If an underwriter sees that a fleet schedule has been normalized, enriched, and compared against appetite rules before review, that is useful. If a claims supervisor sees which open claims have stalled because a medical document is missing, that is useful. If a fraud analyst sees the reason a claim was flagged, plus the supporting data, that is useful.

As boring as it sounds, that makes BI closer to a practical engineering discipline than a reporting project. In engineering, the clever concept is only the start. The real test is whether the thing works under pressure, with constraints, handoffs, deadlines, and real people involved. Insurance BI deserves the same treatment.

The metrics that actually change behavior

A good BI program should not try to measure everything on day one. That is how teams end up with 87 KPIs and no idea which one matters.

Start with metrics that connect directly to action. In underwriting, that might mean submission completeness, quote turnaround, referral rate, re-keying volume, data enrichment hit rate, premium leakage indicators, and bind rate by broker or segment. In claims, it might mean FNOL completion quality, cycle time by claim type, escalation triggers, attorney involvement, fraud flag precision, reserve movement, and customer response time.

The important part is not the metric itself. It is whether someone owns the next step.

If broker submissions are incomplete, who follows up with the broker and changes the intake requirements? If a claims queue has a recurring bottleneck, who fixes routing? If a fraud model is producing too many false positives, who tunes the rules and checks the impact? If policy issuance slows every Friday afternoon, who looks at staffing, document generation, or payment handoffs?

BI that creates accountability gets used. BI that creates trivia gets ignored.

Why BI projects die after launch

Most failed BI projects do not fail dramatically. They fade away quietly, like a New Year's gym membership.

The first reason is timing. If insights arrive after the decision, they become commentary. Insurance teams need leading indicators and near-real-time visibility, especially in high-volume workflows like underwriting intake, FNOL, claims triage, and customer service.

The second reason is generic design. A CFO, an underwriter, a claims adjuster, and a fraud analyst should not all see the same default dashboard. They make different decisions. They need different cuts of the same truth.

The third reason is politics. If each department has its own definitions, dashboards become weapons. One team says the process is fine. Another says the data proves it is broken. Nobody changes anything, but everyone leaves the meeting with a stronger opinion.

The cure is not more charts. It is agreed definitions, shared workflow data, and a review rhythm where teams use BI to run the business, not just explain the past.

A practical playbook for BI teams will use

The first step is to choose one workflow where better visibility would clearly improve speed, accuracy, or leakage. Do not begin with enterprise transformation. Begin with a pain point that the business already complains about in plain English.

Next, define the decisions that workflow requires. For example, an underwriting intake workflow may need to decide whether a submission is complete, whether it fits appetite, whether enrichment is needed, whether it can proceed automatically, and whether it requires human review.

Then capture the operational events behind those decisions. What arrived, when it arrived, what was extracted, what was missing, what rule fired, what system was updated, who touched it, and what happened next. This is where a platform with a data warehouse under the workflow becomes powerful.

After that, enrich the workflow without adding work for the user. Inaza has pre-built API templates that can support enrichment through sources such as Verisk, LexisNexis, HazardHub, and others where appropriate. The goal is not to bury teams in more data. The goal is to bring the right data into the decision without another manual lookup.

Finally, review usage as seriously as accuracy. If the dashboard is correct but nobody uses it, the project is not done. Look at who opens it, where they drop off, which views trigger action, and which metrics are decorative. Yes, decorative metrics are a thing. They are the throw pillows of insurance reporting.

Where Inaza fits

Inaza approaches BI from the workflow outward. The platform automates work across underwriting, claims, customer service, and operations, while capturing the data points created along the way. That data feeds a unified warehouse and can be surfaced through pre-built or custom dashboards.

The practical advantage is that BI is connected to the actual operating process. Teams can deploy customizable workflows, use templates, integrate with existing systems, support multiple file types, and enrich data through ready-made API connections. Inaza also brings benchmarks into the environment, helping insurers compare performance against market reference points and build stronger narratives for portfolio reviews, renewals, and reinsurance discussions.

The important phrase here is teams actually use. If a system requires massive retraining, endless proof-of-concept loops, and a year of governance meetings before anyone sees value, the business will lose patience. Inaza is designed to help insurers move faster, including deploying production-ready workflows quickly and tying the resulting data back into operational intelligence.

For a related angle, the Inaza article on operations observability goes deeper into why seeing every input and output matters for auditability and performance.

Frequently Asked Questions

What is business intelligence in insurance? Business intelligence in insurance is the use of operational, policy, claims, financial, and external data to help teams make better decisions. The best BI supports daily work, such as underwriting prioritization, claims triage, fraud review, portfolio monitoring, and executive reporting.

Why do insurance teams ignore BI dashboards? Teams usually ignore dashboards when the data is late, definitions are unclear, views are too generic, or insights sit outside the workflow. Busy insurance teams use BI when it answers a real question at the moment a decision needs to be made.

Which insurance teams benefit most from BI? Underwriters, claims adjusters, fraud analysts, operations leaders, brokers, MGAs, carriers, and reinsurance teams can all benefit. The key is tailoring the insight to each role instead of giving everyone the same report.

How does automation improve insurance BI? Automation captures clean workflow data as work happens. That gives BI more timely and reliable inputs, including timestamps, exception reasons, handoffs, enrichment results, and decision outcomes. Those signals help leaders see where operations are improving or breaking down.

Can BI help with reinsurance and renewals? Yes. BI can support stronger portfolio narratives by showing performance trends, benchmark comparisons, risk mix, claims development, underwriting discipline, and operational controls. That context can help during reinsurance negotiations and renewal discussions.

Make BI operational, not ornamental

If your BI lives in a separate tab and your teams live in queues, inboxes, and claim files, adoption will always be an uphill battle.

The fix is not another dashboard. The fix is to connect intelligence to the work itself, capture the data that matters as decisions happen, and give each team insight they can act on without becoming part-time analysts.

That is what business intelligence in insurance should be: practical, trusted, timely, and close enough to the workflow that people use it without being asked twice.

If you want to see how Inaza helps insurers turn workflows into usable intelligence across underwriting, claims, customer service, and operations, visit Inaza and start the conversation.