What Good Claim Handling Software Actually Looks Like

Here is my hot take after a decade around claims desks: the best claim handling software is a little boring.

I do not mean dull. I mean dependable. It should not make your claims team feel like they have wandered into a tech conference with lanyards and cold coffee. It should make an ordinary Tuesday at 4:40 p.m., when an adjuster is juggling a water loss, a bodily injury escalation, and a claimant who has called twice, feel manageable.

Good claim handling software does not win because it has the prettiest demo. It wins because it reduces the little frictions that quietly eat your loss ratio, your adjusters’ patience, and your customers’ trust.

I learned this the unglamorous way. Years ago, I watched a perfectly routine auto claim stall for nearly a week because three photos were buried in an email chain, the police report had a spelling mismatch, and the claimant had uploaded a repair estimate as a sideways image. Nothing about the claim was especially complex. The process made it complex. That is the difference good software is supposed to remove.

The first sign of good software: it respects the claim file

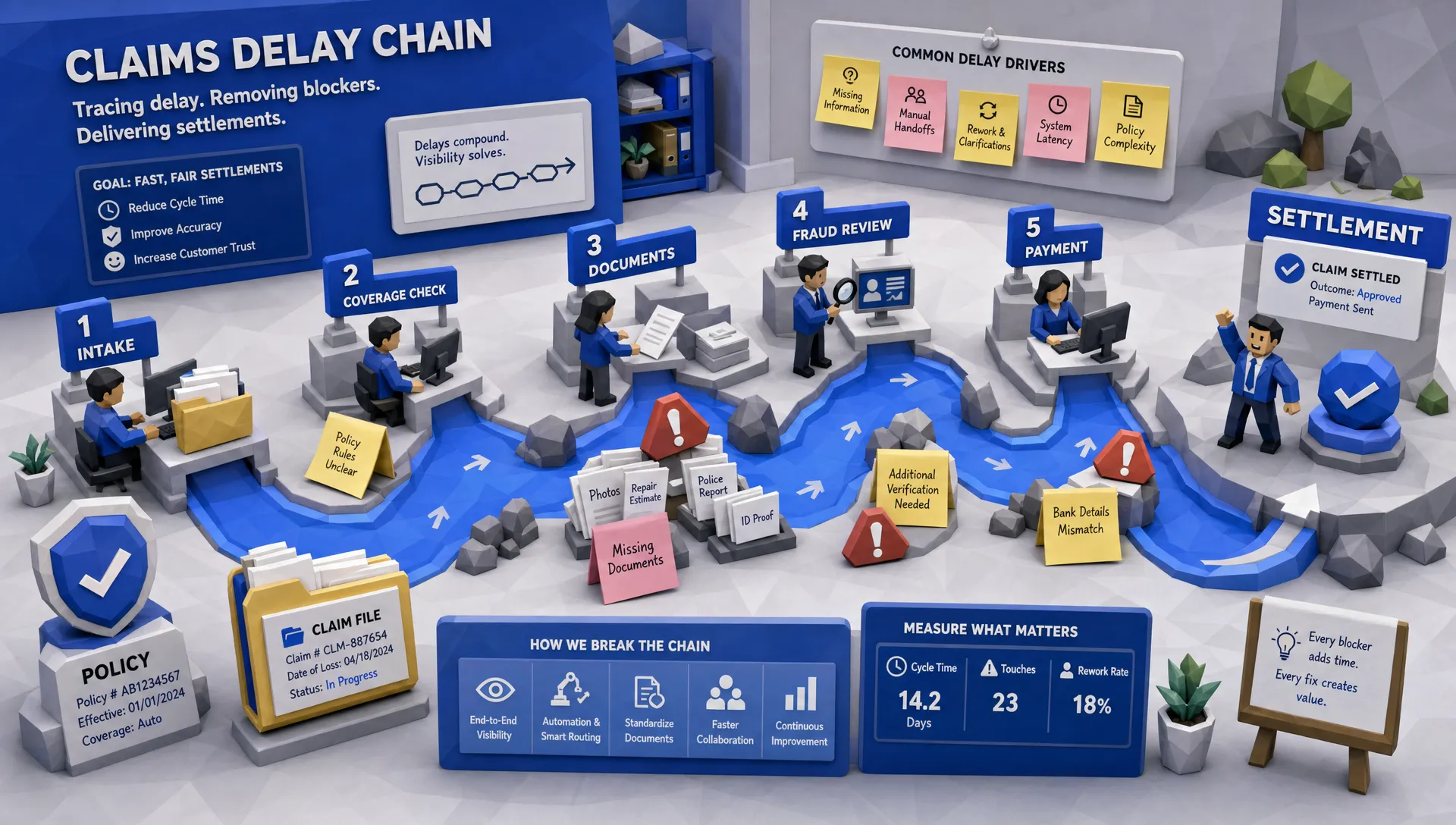

A claim file is not a neat form. It is a pile of half-structured reality.

There are PDFs, photos, emails, invoices, repair estimates, police reports, medical bills, voice notes, handwritten statements, attorney letters, screenshots, weather data, policy documents, and occasionally a file name like IMG_4829_FINAL_FINAL_REAL.pdf. If your claim handling software only behaves well when every field is perfectly completed, it is not ready for real claims work.

Good software can take in the mess and turn it into usable work. It should identify what the file contains, pull out the important facts, flag what is missing, and keep the original evidence tied to the claim. That last part matters. In claims, confidence without evidence is just expensive optimism.

This is also where many systems show their age. They store documents, but they do not understand them. They route tasks, but they do not explain why the task exists. They collect data, but the same data has to be re-keyed later for reporting. That is how rework creeps in wearing a polite little name badge.

If you are actively comparing vendors, this is why I would start with your messiest claims, not the vendor’s clean demo set. Inaza has a practical guide on how to choose insurance claim processing software in 2026, and the same principle applies here: test the system against reality before you fall in love with the interface.

FNOL should feel like intake, not interrogation

First notice of loss is where a claim can become smooth or start limping.

A good FNOL experience asks for the right information at the right time. It does not force a claimant to answer 47 questions before they know whether they are in the correct channel. It does not punish a broker for submitting a PDF. It does not make an adjuster call back just to ask for the date of loss because the field was optional in one portal and mandatory in another.

This may sound basic, but it is where a lot of leakage begins. Missing facts create callbacks. Callbacks create delays. Delays create frustration. Frustration creates complaints, escalations, and sometimes suspiciously creative behavior from people who have been waiting too long.

I sometimes compare claims intake to a good booking page. A salon, contractor, or solo professional needs the page to guide a customer toward the next step without making them think too hard. The same lesson applies to claims portals. If you want a non-insurance example of clear, conversion-focused flow, look at how conversion-focused booking pages for small businesses are built around reducing friction. Claims intake should have that same discipline, even if the stakes are higher than a haircut appointment.

Triage is where the software starts paying for itself

Here is another hot take: triage is more important than the dashboard.

Dashboards are useful, sure. But by the time something appears as red on a dashboard, someone may already be annoyed, delayed, or over-reserved. Strong claim handling software sorts work early. It should know which claims can move quickly, which need human review, which need coverage attention, which need fraud review, and which are likely to become expensive if they sit unattended.

J.D. Power’s 2024 U.S. Auto Claims Satisfaction Study noted that repairable auto claims were taking more than 30 days on average to settle. When you look under the hood, a lot of that time is not heroic investigation. It is waiting. Waiting for documents. Waiting for assignment. Waiting for someone to notice a blocker.

Good triage reduces that waiting. It assigns the right work to the right person, or lets routine claims keep moving with controls in place. It also preserves adjuster judgment. The goal is not to pretend every claim can be fully automated. The goal is to stop making experienced professionals waste half their morning sorting inbox confetti.

A good platform does not pretend every claim is the same

A cracked windshield, a kitchen fire, a soft tissue injury, and a disputed attorney demand should not travel the same workflow. Yet plenty of systems still treat them like cousins at the same family reunion. Technically related, operationally chaotic.

Good claim handling software is configurable by claim type, severity, jurisdiction, coverage, distribution channel, and business rules. A routine physical damage claim may need rapid document capture, estimate validation, and payment controls. A bodily injury claim may need medical chronology, reserve review, litigation watch points, and supervisor visibility. A property claim may need weather enrichment, contractor documentation, and contents handling.

This is why I like the framing in Inaza’s article on why each claim type needs its own workflow. The best claims operations do not chase one universal process. They build a set of controlled pathways that match the actual risk and complexity of the work.

That matters for MGAs and carriers especially. If you are writing multiple products or operating across programs, your claim handling software should not force a one-size-fits-all process because the vendor built the system around a generic claim lifecycle diagram.

The adjuster handoff is where truth comes out

If the software is doing its job, the adjuster should open a claim and immediately understand the situation.

Not after clicking through six screens. Not after searching the document tab. Not after asking a colleague why the system assigned it to their queue. Immediately.

By the time a human handler touches the file, they should be able to see the loss summary, policy and coverage context, key documents, missing information, prior claim indicators, fraud concerns, next recommended action, and why the claim landed in their queue.

That last phrase, why it landed there, is important. Claims teams do not need mysterious automation. They need explainable routing. If a file is marked for supervisor review, the reason should be visible. If it is held for possible fraud review, the signal should be documented. If it is moved forward for fast payment, the controls should be clear.

I once saw a handler decline a fast-track recommendation because she could not tell why the system had suggested it. She was not being difficult. She was being professional. If you cannot explain the recommendation, you cannot expect the adjuster to trust it.

Fraud checks need to be early, quiet, and explainable

Fraud detection should not feel like airport security for every claimant. Most customers are honest and already having a bad day. But the system still needs to be sharp.

The fraud environment is getting stranger. Verisk’s 2025 fraud report points to rising concern around digitally altered materials and synthetic evidence, with carriers reporting that new tools are changing the fraud landscape. We have also seen more scrutiny around generated images, manipulated documents, and repeat patterns across claims.

Good claim handling software screens early without turning every claim into a confrontation. It can compare facts, spot inconsistencies, check prior loss history through appropriate data sources, enrich with third-party information, and preserve a clear audit trail. The key is not simply flagging more claims. The key is flagging better, with fewer false positives and better documentation.

A fraud flag that says suspicious is not very helpful. A fraud flag that says the vehicle damage photo appears inconsistent with the reported impact location, the claimant has two similar losses in 18 months, and the repair invoice metadata does not match the stated date is much more useful.

Reporting should come from the work, not after the work

One of my least favorite claims rituals is the end-of-month reporting scramble. Everyone knows the numbers are needed. Everyone also knows some of the numbers are being reconstructed from fields that were not captured cleanly in the first place.

Good claim handling software captures operational data as the work happens. That means the system can show where claims are stuck, which documents are most often missing, which handlers or vendors are overloaded, which claim types drive rework, how reserves are changing, and where leakage may be forming.

This is where a data warehouse underneath the workflow matters. Workflow automation is useful, but the real long-term value comes from turning claims activity into business intelligence. If the system knows why claims were delayed, not just that they were delayed, leaders can fix the process instead of giving another speech about urgency.

Celent has written about straight-through processing in claims, and industry adoption remains much lower than people outside claims might assume. That should not surprise anyone who has handled real files. Many claims need judgment. But even when a claim cannot go straight through, the surrounding data should still be captured cleanly.

If you want a deeper look at the operational side, Inaza’s article on how insurance claims software can cut rework and cycle time is worth pairing with this one. Rework is not usually one big mistake. It is ten tiny avoidable repeats.

Integrations should reduce swivel-chair work

No claims team has ever said, please give me another screen to check.

Good claim handling software integrates with the systems your team already uses: policy administration, billing, document management, payment systems, fraud tools, repair networks, data providers, communication channels, and reporting environments. The point is not to create a shiny island. The point is to remove swivel-chair work.

This is also where pre-built API templates can save a lot of time. If a claims workflow needs enrichment from providers such as Verisk, LexisNexis, HazardHub, or other data sources, the software should make that practical without a long custom build every time. The more your team can enrich, validate, and route claims inside the workflow, the less they depend on manual checking.

For insurers, MGAs, and brokers, integration also affects adoption. If handlers need to abandon their natural process to serve the software, they will work around it. And claims people are very good at workarounds. Give an adjuster a clunky system and a spreadsheet will appear by lunch.

The best systems can be changed without a six-month committee

Claims operations change constantly. New fraud patterns appear. Capacity shifts. A carrier changes authority levels. A program adds a jurisdiction. A reinsurer asks better questions. A storm season makes your neat operating model look adorable.

Good claim handling software can adapt. Business users should be able to adjust workflows, rules, routing, templates, and dashboards without entering vendor ticket purgatory. There should still be governance, approvals, and audit trails. Flexibility without control is just chaos in better shoes.

This is one of the reasons we take workflow deployment seriously at Inaza. The value is not in building a beautiful proof of concept that never survives contact with operations. The value is in getting production-ready workflows live quickly, then capturing the data needed to improve them.

If a vendor needs months to show value on one practical claims workflow, ask yourself what will happen when the business changes three workflows at once.

My practical test for claim handling software

When I help teams think through claim handling software, I always suggest the same test: bring ugly examples.

Do not bring the clean claim with perfect fields and friendly documents. Bring the claim where the claimant used three email addresses. Bring the claim with a coverage question. Bring the total loss with lienholder confusion. Bring the property loss with photos, contractor estimates, weather questions, and a suspicious invoice. Bring the attorney demand that arrived as a 42-page PDF at 4:58 p.m. on a Friday, because of course it did.

Then ask the vendor to show how the software handles intake, document capture, triage, enrichment, routing, adjuster handoff, fraud signals, customer communication, supervisor review, payment controls, and reporting.

You will learn more in that hour than in three polished demos.

What you want to see is not perfection. You want to see the software fail gracefully. Does it ask for missing information? Does it preserve evidence? Does it route exceptions? Does it explain decisions? Does it make the next step obvious? Does it capture data for reporting without asking the adjuster to become a part-time data clerk?

If yes, you may have something real.

What good looks like day to day

Good claim handling software changes the feel of the claims floor.

Customers get clearer updates. Adjusters spend less time hunting and more time deciding. Supervisors see bottlenecks before they become complaints. Fraud analysts get better leads, not just more noise. Operations teams can compare performance across programs and claim types. Executives can see what is actually driving cycle time, cost, and leakage.

And perhaps most importantly, the claims team trusts the system because it reflects their work. It does not flatten professional judgment into a checkbox. It supports judgment with cleaner data, better routing, and fewer avoidable distractions.

That is what good looks like. Less drama. Fewer mystery delays. Better evidence. Cleaner handoffs. Faster resolution when appropriate, deeper review when needed.

Not glamorous. Very profitable.

Frequently Asked Questions

What is claim handling software? Claim handling software helps insurers, MGAs, brokers, and adjusters manage the operational work of a claim, including intake, document capture, triage, assignment, communication, fraud checks, payments, reporting, and audit history.

How is claim handling software different from claim processing software? The terms overlap, but claim handling software usually focuses on the day-to-day work of managing claims from FNOL to resolution. Claim processing software may refer more narrowly to workflow steps, payments, or administrative processing.

Can claim handling software automate complex claims? It can automate parts of complex claims, such as document intake, enrichment, reminders, fraud screening, and reporting. The best systems do not remove human judgment from complex files. They give adjusters cleaner information and better controls.

What metrics should good claim handling software track? At minimum, it should track cycle time, touch time, rework, missing documentation, claim aging, reserve changes, escalation rates, fraud referrals, customer communication, vendor performance, and outcomes by claim type.

Does better claim handling software replace adjusters? No. Good software reduces administrative drag so adjusters can focus on decisions, negotiation, coverage analysis, customer communication, and complex claim handling. In my experience, that is where experienced people create the most value.

Make claim handling less painful

If your claims operation is still relying on manual intake, disconnected systems, and heroic adjuster memory, the problem is not your people. The workflow is carrying too much friction.

Inaza helps insurers, MGAs, and brokers automate claims workflows, connect data across systems, enrich files through integrations, and turn claims activity into useful operational insight. Good claim handling software should make real work easier, and that is the standard worth holding vendors to.