Insurance Software Solutions That Fix Workflow Bottlenecks

Here is my slightly spicy view after a decade around underwriting desks, claims teams, and more shared inboxes than any human should endure: most insurance workflow bottlenecks are not caused by lazy teams or bad processes. They are caused by software that asks smart people to behave like copy-paste machines.

I once watched an experienced underwriter spend 20 minutes hunting through three PDFs, one broker email, and a spreadsheet named “final_final_v7.xlsx” just to confirm a VIN and prior loss detail. The risk was not complicated. The workflow was.

That is the real test for modern insurance software solutions. They should not simply digitize the mess. They should remove the moments where work gets stuck, duplicated, re-keyed, questioned, rerouted, or forgotten.

And yes, I know every vendor says they “streamline operations.” That phrase has carried more weight than a claims file from 1998. So let’s get practical. What bottlenecks should insurance software actually fix, and what should carriers, MGAs, brokers, reinsurers, adjusters, fraud teams, and underwriters look for before signing another platform contract?

The bottleneck is usually hiding in the handoff

In insurance, we love to blame the obvious backlog. The underwriting queue. The pending claims folder. The unanswered customer emails. The attorney demand deadline that appeared like a raccoon in the attic, loud, inconvenient, and somehow already expensive.

But the visible queue is usually the symptom. The cause is often a handoff that relies on manual interpretation.

A broker sends a submission. Operations extracts the data. Underwriting validates it. Someone checks third-party sources. Someone else asks for missing documents. The underwriter reviews the risk. A referral goes to a senior underwriter. A quote gets generated. Then someone updates the policy admin system.

Each handoff creates a small tax. Sometimes it is a time tax. Sometimes an error tax. Sometimes a “who owns this now?” tax, which might be the most expensive one of all.

McKinsey has reported that underwriters can spend a large share of their time on administrative activities rather than risk selection and pricing, which tracks with what I have seen on the floor. Smart people are reviewing attachments, re-entering fields, comparing documents, and chasing missing data when they should be deciding whether the account makes sense.

The same happens in claims. A First Notice of Loss lands, documents arrive later, images need checking, invoices need review, fraud indicators need routing, coverage needs confirming, and customer updates need sending. If those steps live in disconnected tools, even a straightforward claim starts to feel like a relay race where every runner has to fill out a form before passing the baton.

What good insurance software solutions should fix first

My hot take: the best insurance software does not start by promising full transformation. It starts by killing one painful bottleneck so cleanly that the team wants to automate the next one.

The fastest wins usually come from fixing these workflow choke points:

- Intake chaos across emails, PDFs, spreadsheets, portals, images, and attachments

- Manual data entry and re-keying between systems

- Slow enrichment from third-party data providers

- Referral queues with unclear ownership or incomplete context

- Claims triage that depends on human sorting before any real decision happens

- Fraud review processes that create too many false positives or miss early warning signs

- Reporting that arrives after the operational problem has already grown teeth

That last one matters more than people admit. If you only know where the bottleneck was at the end of the month, you are not managing operations. You are reading the autopsy.

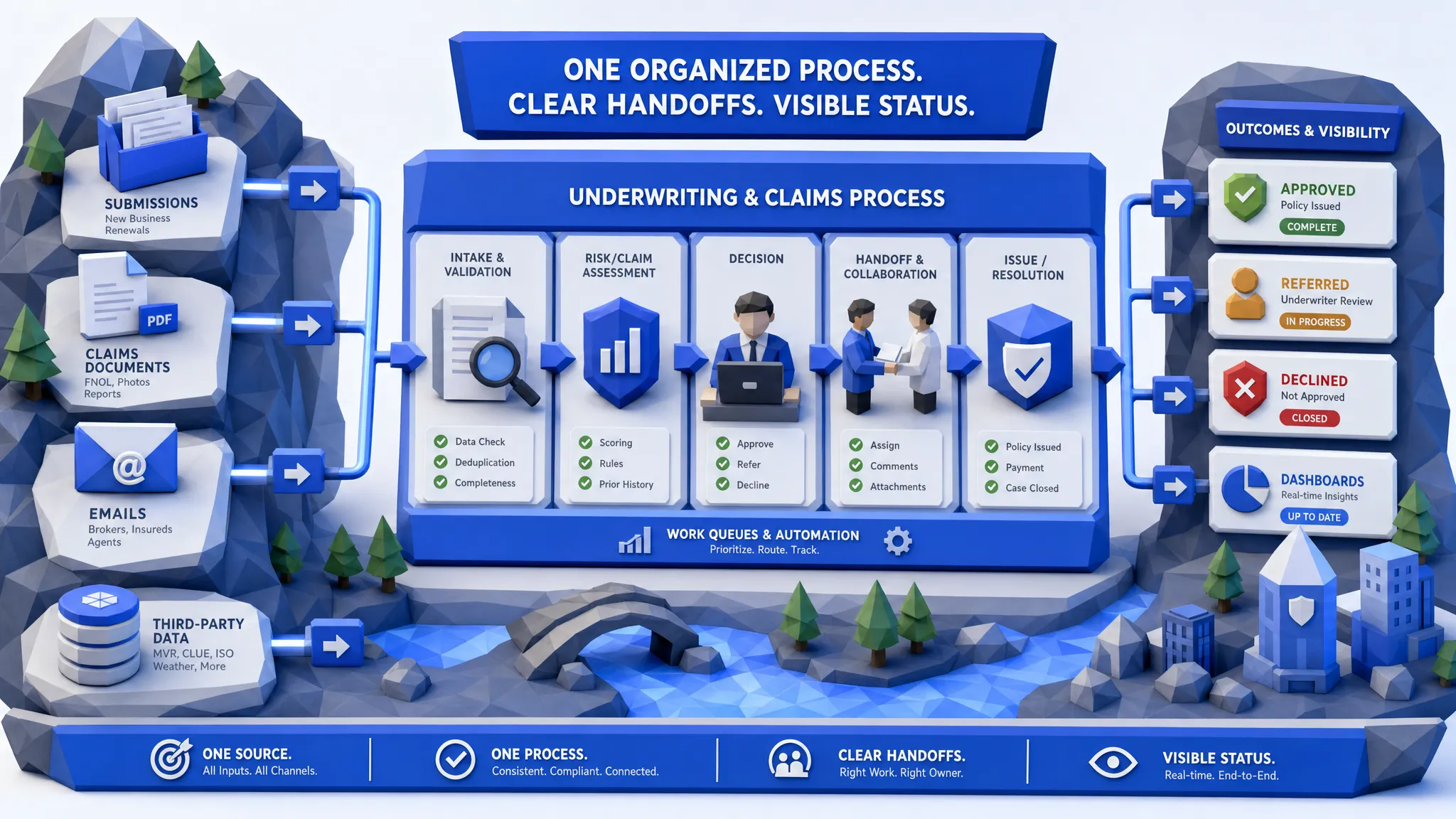

Intake automation: stop treating every document like a special snowflake

Every insurer has some version of the same intake problem. Broker submissions arrive in different formats. Loss runs vary by carrier. Fleet schedules are messy. Claims documents come in as PDFs, photos, scanned forms, emails, and sometimes, if the universe is feeling mischievous, screenshots inside Word documents.

A proper insurance automation platform should support all file types and extract the data into a consistent structure. Not “we can OCR it and hope for the best.” I mean it should understand the insurance context, normalize fields, validate what is missing, and push the right data into downstream workflows.

This is where workflow bottlenecks often start. If the first step is messy, every later step inherits that mess.

For underwriting, intake automation means submissions can be reviewed faster because underwriters are not assembling the file from scratch. For claims, it means FNOL details, photos, invoices, and supporting documents can be organized before an adjuster touches the file. For operations, it means fewer emails asking, “Can someone confirm whether this is the latest version?”

If your team is still manually entering the same data into multiple systems, you are paying twice for the same work and getting an error risk as a bonus prize. We have written more about this in our piece on eliminating re-keying across the insurance lifecycle.

Underwriting bottlenecks: the underwriter should decide, not assemble

Underwriters are not expensive because they type quickly. They are expensive because they understand risk.

The problem is that many underwriting workflows still treat underwriters like human middleware. They gather information from one system, check another, compare it to guidelines, ask for missing documents, validate eligibility, and only then get to the actual underwriting judgment.

Good underwriting software should remove that assembly work. It should capture the submission, extract key fields, validate them, enrich the file through trusted sources, apply your underwriting rules, and route the case based on risk and authority.

This is especially important for MGAs and commercial auto teams where volume and variability collide. A single fleet submission might include vehicle schedules, driver lists, garaging locations, loss runs, prior coverage, and odd formatting choices that suggest someone lost a bet with Excel.

The right platform should not force underwriters to learn an entirely new way of working. It should integrate with existing systems and make the current workflow faster, cleaner, and more visible. That is one reason Inaza is designed around configurable workflows, pre-built templates, and integrations rather than a rip-and-replace approach.

There is also a growth angle here. Brokers and MGAs can invest in marketing, referrals, and even partners that help book qualified B2B sales calls, but if submission intake and quote turnaround are slow, demand turns into quote abandonment. A faster front door means very little if the back office is carrying sandbags.

Claims bottlenecks: speed is a customer experience issue and a leakage issue

Claims teams live under a different kind of pressure. Underwriting delays are frustrating. Claims delays are personal.

When a policyholder has an accident, a damaged vehicle, or a loss that disrupts their life, every extra day feels bigger. J.D. Power’s claims research consistently shows how strongly the claims experience affects satisfaction, and anyone who has handled auto claims knows the pattern: the longer the uncertainty lasts, the more calls come in, the more frustration rises, and the more expensive the file can become.

The workflow bottleneck in claims is often early triage. Is the claim simple or complex? Is coverage clear? Are the photos valid? Is there injury involvement? Is an attorney already involved? Is the invoice consistent with the damage? Does the claim need SIU review?

If those questions wait for manual review, the claim is already losing time.

Claims automation should collect FNOL data, organize documents, check images, validate invoices, surface fraud flags, and route files based on severity and complexity. It should also know when a human needs to step in. I am a strong believer in automation for routine claims, but I am also old enough to know that a grieving customer, a disputed bodily injury file, or a suspicious claim should not be handled like a pizza order.

The goal is not to remove adjusters. The goal is to stop wasting adjuster time on work that software can prepare, summarize, and route.

Fraud bottlenecks: false positives are their own kind of waste

Fraud detection is one of those areas where bad software can create the illusion of control. If a system flags everything, it looks busy. It also buries your fraud analysts in noise.

The FBI notes that non-health insurance fraud costs more than $40 billion per year in the United States, excluding health insurance. That is a real number with real consequences for loss ratios, premiums, and customer trust.

But a fraud workflow bottleneck does not only happen when fraud is missed. It also happens when legitimate claims are over-flagged. Every false positive pulls an adjuster, analyst, or investigator into unnecessary review. Worse, it can slow down good customers who did nothing wrong.

Modern fraud-focused insurance software should combine multiple signals before escalating a case. For example, image metadata, document consistency, claim history, repair invoices, prior loss patterns, and behavioral indicators are more useful together than in isolation.

The practical win is better routing. Low-risk claims move faster. Suspicious claims get reviewed earlier. Analysts spend less time clearing obvious false alarms and more time investigating cases that deserve attention.

The overlooked bottleneck: no one can see the whole operation

Here is the bottleneck I think gets underfunded: visibility.

Most insurers can tell you how many claims are open or how many submissions are pending. Fewer can tell you, in real time, which step is causing the delay, which data field is most often missing, which broker submissions require the most rework, which adjuster queues are overloaded, or how their operational performance compares with market benchmarks.

That is where a data warehouse becomes more than an IT project. It becomes an operating advantage.

Inaza’s platform has a unified data warehouse underneath the workflows. That matters because every automated step can capture structured data. Instead of automation being a black box that simply moves work along, it becomes a source of business intelligence.

For insurers, MGAs, and brokers, this can support dashboards for turnaround time, referral rates, missing data, claim severity, leakage indicators, fraud flags, and operational throughput. For reinsurers and reinsurance brokers, benchmarked portfolio narratives can support renewals and treaty discussions with more confidence.

Inaza also includes industry benchmarks from sources such as Aon, Munich Re, and Howden. That context is valuable because internal performance alone can be misleading. A 24-hour underwriting SLA sounds great until you realize peers are clearing similar cases in four hours. Or perhaps your team is better than market and should be using that story in partner conversations.

What to ask before choosing insurance software

If I were evaluating insurance software solutions today, I would worry less about the slickest demo and more about how the system behaves on an ugly Tuesday afternoon.

Ask these questions before you buy:

- Can the platform handle the real files we receive, including messy PDFs, spreadsheets, emails, images, and inconsistent formats?

- Can it integrate with our existing core systems, claims systems, CRM, rating tools, and data providers?

- Can business users configure workflows without months of vendor back-and-forth?

- Does it capture operational data for reporting and analytics, or does it only move tasks around?

- Can it explain decisions, routing, exceptions, and audit trails clearly enough for compliance and management review?

- Can it start with one high-impact workflow and scale across underwriting, claims, customer service, and operations?

That last question is important. I have seen too many teams spend a year planning a transformation program before fixing even one bottleneck. By then, the market has moved, the backlog has grown, and the project steering committee has developed its own gravitational field.

Start smaller. Prove value. Expand fast.

Where Inaza fits in the workflow bottleneck problem

Inaza is built for insurers, MGAs, and brokers that want automation without tearing out the systems they already depend on.

The platform supports underwriting automation, claims process automation, customer service automation, operational workflows, reporting, and analytics. It integrates with existing systems, captures data across workflows, and turns that activity into real-time dashboards. It also supports all file types, which is useful because insurance operations rarely receive documents in the neat format we wish they did.

A few Inaza capabilities matter specifically for bottlenecks:

- 250+ workflow templates to accelerate deployment

- Customizable automation workflows for underwriting, claims, service, and operations

- Pre-built API templates for data enrichment, including providers such as Verisk, LexisNexis, and HazardHub

- A unified data warehouse that captures workflow data for analytics and reporting

- Real-time dashboards for operational visibility

- Industry benchmarks that help compare performance against market context

- Deployment designed to avoid long proof-of-concept cycles and unnecessary team retraining

That combination is the difference between “we automated a task” and “we improved how the business runs.”

To be blunt, if your software cannot tell you where work is stuck, why it is stuck, and how often it gets stuck, it is not fixing the bottleneck. It is decorating it.

Frequently Asked Questions

What are insurance software solutions? Insurance software solutions are platforms or tools that help insurers, MGAs, brokers, and claims teams manage workflows such as underwriting, claims, policy servicing, customer communication, fraud detection, reporting, and data integration.

Which workflow bottlenecks should insurers automate first? Start with bottlenecks that combine high volume, manual effort, and measurable delays. Common examples include submission intake, loss run extraction, FNOL triage, claims document review, invoice validation, eligibility checks, and broker email routing.

Do insurance software solutions need to replace core systems? Not necessarily. Many modern platforms are designed to integrate with existing systems through APIs and connectors. For most insurers, incremental automation is less risky and faster to prove than a full core replacement.

How does automation improve underwriting workflows? Automation helps collect submission data, structure documents, enrich risk information, apply rules, identify missing details, and route cases to the right underwriter. This lets underwriters spend more time on judgment and less time on administrative work.

How does workflow automation help claims teams? Claims automation can speed FNOL intake, organize supporting documents, validate images and invoices, identify fraud indicators, route claims by severity, and trigger customer updates. The result is faster handling for routine claims and earlier escalation for complex ones.

What should insurers look for in an automation platform? Look for integration flexibility, support for messy real-world files, configurable workflows, strong audit trails, analytics dashboards, data enrichment options, and the ability to start with one workflow before scaling across the business.

Ready to remove the bottleneck instead of managing around it?

If your teams are spending too much time chasing documents, re-keying data, clearing queues, or explaining why work is delayed, the problem may not be headcount. It may be the workflow.

Inaza helps insurers, MGAs, and brokers automate underwriting, claims, customer service, and operations while keeping existing systems in place. If you want to see where your workflows are stuck and how quickly they can be improved, get in touch with Inaza and let’s talk through the bottleneck that is costing you the most time right now.