Why Delayed Insurance Claims Usually Start Earlier Than You Think

Here is my hot take: most delayed insurance claims are not really delayed in claims.

They are delayed in the quote. In the binder. In the way documents are received. In the first phone call. In the “we’ll figure that out later” field that nobody wanted to make mandatory because it might annoy the broker.

By the time a customer is asking, “Where is my payment?”, the delay has often been quietly aging in the file for days, sometimes weeks. Claims gets the angry email, of course. Claims always gets the angry email. But the root cause is usually upstream.

I learned this the unglamorous way years ago on a commercial auto file. Everyone blamed the adjuster because the claim sat untouched for three days. When we opened the file, the adjuster had actually done the sensible thing: stopped. The listed vehicle did not match the VIN, the driver was missing from the schedule, and the policy documents were split across three systems. It was not a lazy adjuster problem. It was a “we built a scavenger hunt and called it a workflow” problem.

That is why delayed insurance claims deserve a broader diagnosis. If we only measure the pain from first notice of loss onward, we miss the operating habits that created the delay in the first place.

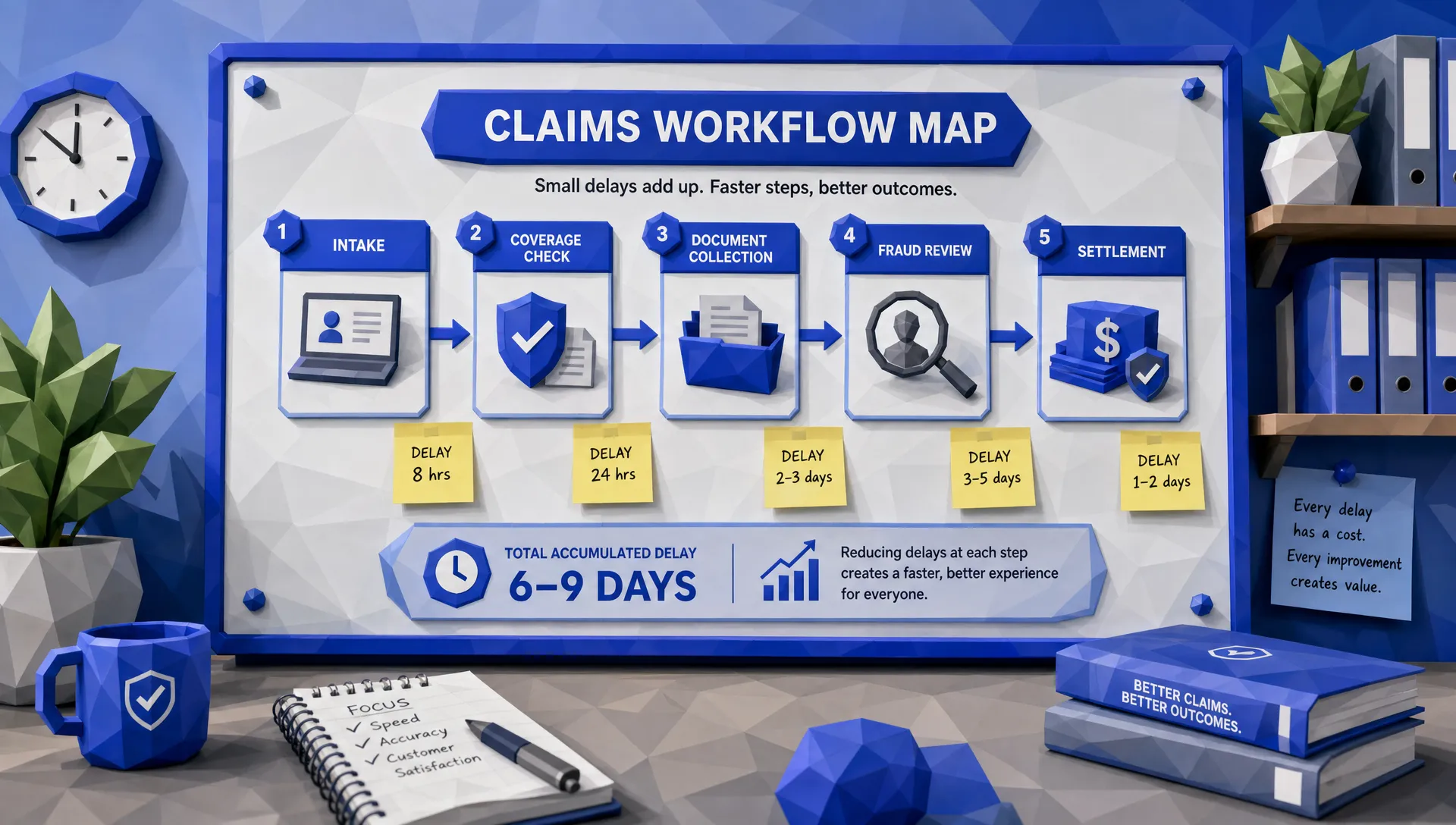

The delay clock starts before FNOL

First notice of loss gets treated like the starting gun. In reality, it is more like the moment the smoke alarm goes off. The issue may have started much earlier.

A claim can only move quickly if the policy, risk, parties, coverage, and evidence are easy to verify. If underwriting data is incomplete, if policy documents are buried in PDFs, if endorsements are unclear, or if key risk attributes were never captured in a structured way, claims teams inherit friction.

This is where I think insurers often fool themselves. They ask, “Why did this property claim take 26 days?” Then they look only at the adjuster notes. They do not ask why occupancy data was inconsistent at bind. They do not ask why the insured’s contact details were stale. They do not ask why the broker submission included five attachments with overlapping information and no clean data trail.

McKinsey has written that underwriters can spend a huge share of their time on administrative work rather than risk assessment. That admin burden is not only an underwriting productivity problem. It becomes a claims speed problem later, because claims depends on the same information being accurate, accessible, and usable.

If underwriting is entering, copying, interpreting, and reinterpreting data manually, claims will eventually pay the bill. Sometimes literally.

FNOL is where earlier sins become visible

FNOL is supposed to collect the facts. Too often, it collects confusion.

I once reviewed a household water damage claim where the customer gave a perfectly reasonable report: “Pipe burst under the sink, floor is soaked.” Simple enough. But the FNOL form did not ask whether the water was still running, whether emergency mitigation had begun, whether photos were available, or whether the property was occupied. The handler had to call back. Then the vendor had to call. Then coverage needed clarification. By Monday morning, the “simple” claim had become a queue resident.

That delay did not start when the adjuster picked up the file. It started when the intake process failed to ask the questions the next person needed answered.

Claims operations are a bit like packaging a fragile item. If the item is put in the wrong box, the damage shows up during shipping, not at the packing table. Companies that specialize in custom corrugated packaging obsess over fit, handling, and purpose before the box leaves the building. Claims should be treated the same way. The quality of the container at intake determines how safely and quickly the file travels through the process.

That does not mean FNOL needs to become a courtroom deposition. Nobody wants a customer with a cracked windshield to answer 47 questions and upload a notarized sketch of the parking lot. It means intake should be adaptive. A theft claim needs different questions than a rear-end collision. A litigated bodily injury demand needs different routing than a low-severity property claim.

The best FNOL process is not the longest one. It is the one that gives the next decision-maker what they need without creating customer friction.

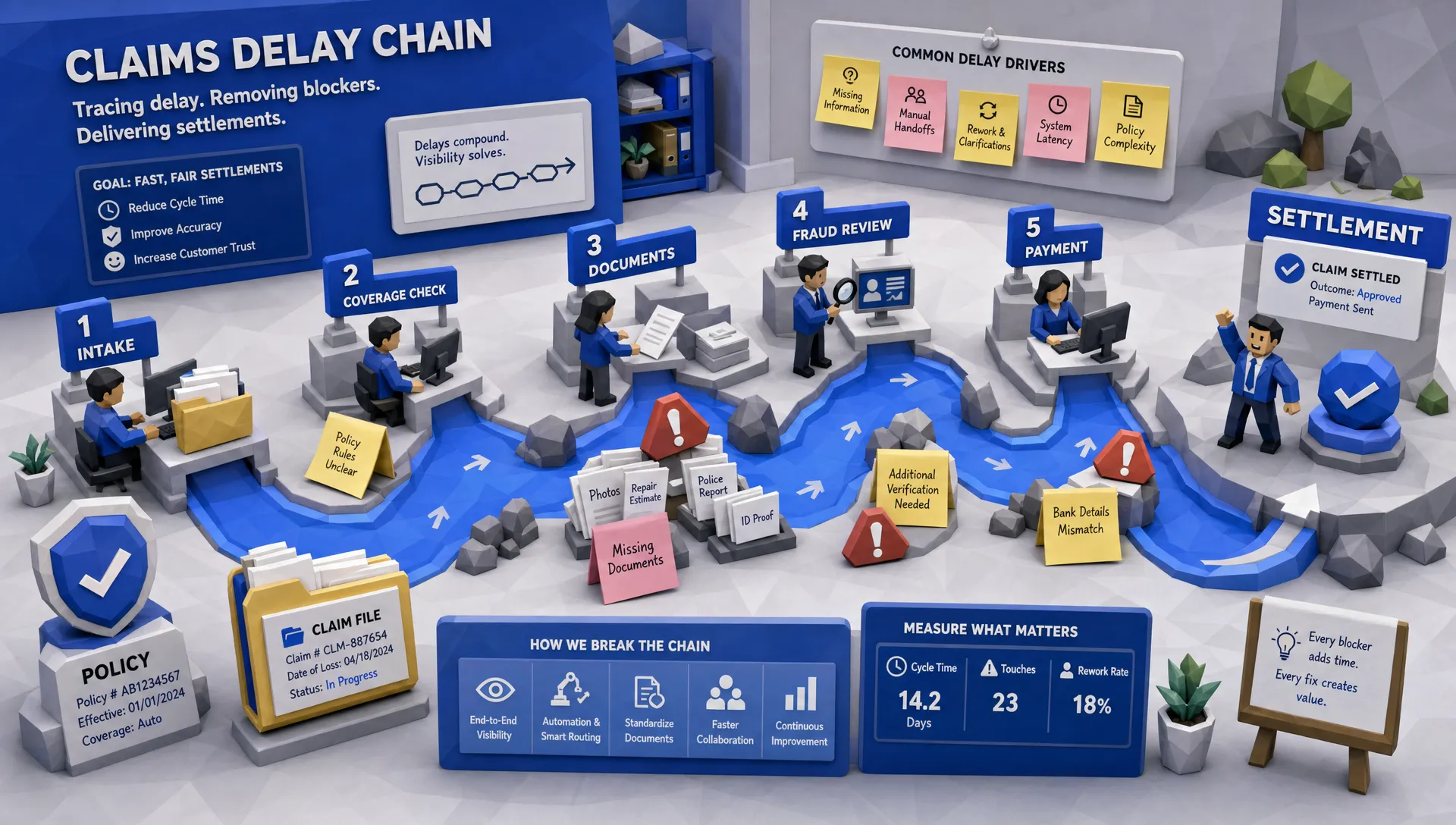

The hidden waiting rooms inside delayed insurance claims

Every claims team has obvious queues. New claims. Pending documents. Supervisor review. Payment approval. But the real delays are often hiding between those queues, in the little pauses nobody owns.

A file waits for coverage confirmation. Then it waits for a missing photo. Then it waits for a liability decision. Then it waits because the estimate format does not match what the carrier needs. Then it waits for fraud review, legal review, or a manager who is already in six meetings.

None of those pauses look dramatic in isolation. Together, they become the reason a customer calls three times in one week.

J.D. Power’s 2024 U.S. Auto Claims Satisfaction Study noted that auto claims can still take more than 30 days on average to settle, depending on the circumstances, and customers feel every extra day. The lesson is not simply “work faster.” Adjusters already work fast, and most of them are juggling more context than any dashboard admits. The lesson is to remove waiting states that do not add judgment, protection, or value.

If a claim is waiting because a person must evaluate liability, that is real work. If a claim is waiting because someone has to retype a policy number from an attachment, that is waste wearing a tie.

Fraud checks should not arrive like a plot twist

Fraud prevention is one of the most common reasons people defend slower claims processes. Fair enough. We do not want to pay bad claims quickly. That is not innovation, that is donating.

But fraud checks cause the most damage when they arrive late. If a suspicious loss indicator is only discovered after liability work, vendor activity, and customer updates have already moved forward, the claim gets pulled backward. That creates rework, awkward conversations, and longer cycle times.

Fraud screening works better when it happens early and quietly in the normal flow of the claim. The goal is not to treat every customer like a suspect. The goal is to identify the small number of files that need more attention before the team has invested time in the wrong path.

The pressure is rising. Verisk’s 2025 fraud research points to growing concern among carriers about digitally enabled fraud, including manipulated images and synthetic evidence. The FBI has also long warned that insurance fraud costs consumers and insurers billions each year. For claims leaders, the takeaway is practical: fraud controls need to be embedded early enough to prevent delay, not bolted on late enough to create it.

We have written before about where insurance claim fraud detection pays off fastest, and my view is the same here. Fraud detection should not be a separate island. It should be part of the route map.

The handoff is where good claims go to nap

If I had a dollar for every claim delayed by a handoff, I would have retired somewhere warm and become annoyingly interested in sailing.

Handoffs are dangerous because they feel normal. A file moves from intake to coverage. From coverage to liability. From liability to estimate review. From estimate review to payment. Each step makes sense. The trouble starts when context does not travel with the file.

One team sees the broker notes. Another sees the policy record. Another sees the images. Another sees the payment screen. Everyone has a slice of the truth, and the adjuster becomes the person trying to assemble the full sandwich.

This is why I am skeptical of claims improvement projects that focus only on one screen or one task. A faster document review tool helps, but if the output still gets emailed to a shared inbox, congratulations, you have built a faster way to create another queue.

The better approach is connected data. When policy data, FNOL details, documents, fraud signals, vendor updates, and payment status are visible in one operating flow, teams spend less time asking “what happened?” and more time deciding “what should happen next?” That is the same argument we make in our piece on why insurance claims services work better with connected data.

Delayed claims are an underwriting issue too

This is the part some claims leaders love and some underwriting leaders pretend not to hear: claims delays often expose underwriting data weaknesses.

Think about commercial property. If the construction type, occupancy, protection class, roof details, or location data are unclear, the claim may need extra coverage review. Think about personal auto. If drivers, garaging address, vehicle use, or prior damage records are incomplete, the claim slows down while the team checks what should have been clear. Think about specialty lines. If schedules, endorsements, limits, or exclusions are trapped in documents rather than structured fields, every claim becomes a mini archaeology project.

This does not mean underwriting caused the claim. It means underwriting and claims share the same data foundation. When that foundation is messy, the crack may only become visible after a loss.

For MGAs and carriers, this matters beyond claim handling. Claims data feeds pricing, reserving, reinsurance discussions, renewal strategy, broker performance analysis, and portfolio management. If the claims process is full of manual interpretation and missing context, the business intelligence that comes out of it will be weaker too.

That is why I like looking at delayed insurance claims as a data lifecycle problem, not just a service-level problem. A delay is often a symptom that the organization cannot move facts cleanly from one decision to the next.

What I would fix first

If your claims are already slow, the temptation is to start at the end: settlement authority, payment approvals, closing notes. Those areas matter, but I would start earlier.

First, I would look at the first 15 minutes of the claim. What information is captured? What is missing? Which fields are free text when they should be structured? Which claim types get routed the same way even though they clearly need different treatment?

Second, I would inspect the first handoff. Does the next person receive the full context, or do they have to reconstruct it? If the answer is “they check three systems and maybe an email thread,” there is your delay.

Third, I would measure wait time by status. Average cycle time is useful, but it can hide the ugly bits. A claim may look like it took 18 days, but the real story is that 9 of those days were spent waiting for information nobody requested properly on day one.

Fourth, I would connect claims feedback to underwriting. If claims teams repeatedly struggle with the same policy ambiguity, missing data point, or document format, that should influence submission intake, underwriting workflows, and broker requirements.

Finally, I would stop treating automation as a grand transformation project that needs twelve steering committees and a commemorative mug. Some of the best improvements are practical: capture data once, enrich it automatically where appropriate, route files based on rules, surface exceptions early, and give teams dashboards that show where work is actually stuck.

For a deeper look at the operational side, our article on how insurance claims software cuts rework and cycle time breaks down how better intake, triage, handoffs, and data flow reduce avoidable delays.

Where Inaza fits into the problem

At Inaza, we see delayed claims as a workflow and data problem before we see it as a staffing problem. More people can help in peak periods, of course. But if the process is asking skilled people to chase documents, rekey data, and reconcile systems, adding headcount just spreads the friction around.

Inaza’s insurance automation platform is designed to help insurers, MGAs, and brokers streamline workflows across underwriting, claims, customer service, and operations. The practical value is in connecting the work: capturing data from files and systems, integrating with existing tools, automating repeatable steps, and turning those workflow outputs into reporting and analytics.

The data warehouse matters here. If every automated workflow also captures useful operational data, leaders can see where delays begin, not only where they become embarrassing. That is how you move from “our claims feel slow” to “commercial auto claims with missing driver data spend 4.2 extra days in coverage review.” One is a complaint. The other is a fixable business problem.

Frequently Asked Questions

What causes delayed insurance claims? Delayed insurance claims are usually caused by missing information, unclear coverage, manual handoffs, late fraud checks, disconnected systems, or poor intake. The visible delay may happen in claims, but the root cause often begins earlier in underwriting, policy administration, or FNOL design.

Are delayed insurance claims always the adjuster’s fault? No. Adjusters often inherit delays created by incomplete data, unclear documents, fragmented systems, or weak routing rules. Blaming adjusters may feel satisfying for about five minutes, but it rarely fixes the process.

How can insurers reduce claim delays without weakening fraud controls? The best approach is to screen for fraud indicators early, route suspicious files quickly, and let clean claims move without unnecessary friction. Fraud controls should be built into the workflow rather than added late in the process.

Why does underwriting data affect claims speed? Claims teams rely on policy and risk data to confirm coverage, validate parties, assess limits, and understand exclusions. If that information is incomplete or trapped in unstructured documents, the claim slows down while people investigate what should already be clear.

Where should an MGA start if claims cycle time is too long? Start with FNOL quality and the first handoff. Look at what information is captured, what is missing, how claims are routed, and how much time files spend waiting between steps. Those early moments often explain the delays customers feel later.

Stop finding delays after your customers do

Delayed insurance claims rarely come from one dramatic failure. They come from small moments of friction that compound: a missing field, a vague note, a late fraud flag, a disconnected system, a handoff without context.

The good news is that those moments can be redesigned.

If you want to reduce claims delays without asking your teams to sprint harder on a broken track, Inaza can help you automate workflows, connect data, and see where claims are getting stuck before customers start chasing updates. The earlier you find the delay, the easier it is to remove it.